CapitaLand Malaysia Mall Trust (Oct 24, RM1.55)

Maintain hold with a target price of RM1.65: CapitaLand Malaysia Mall Trust’s (CMMT) management is focusing its efforts to arrest rental reversion decline for Sungei Wang Plaza (SWP) and has put in place strategies to help reposition and rebrand the mall.

Nonetheless, we believe that this would only bear fruit in the longer term with the completion of the Mass Rapid Transit (MRT) in the second half of 2017. Contributions from its other malls should help offset the weakness from SWP in the medium term.

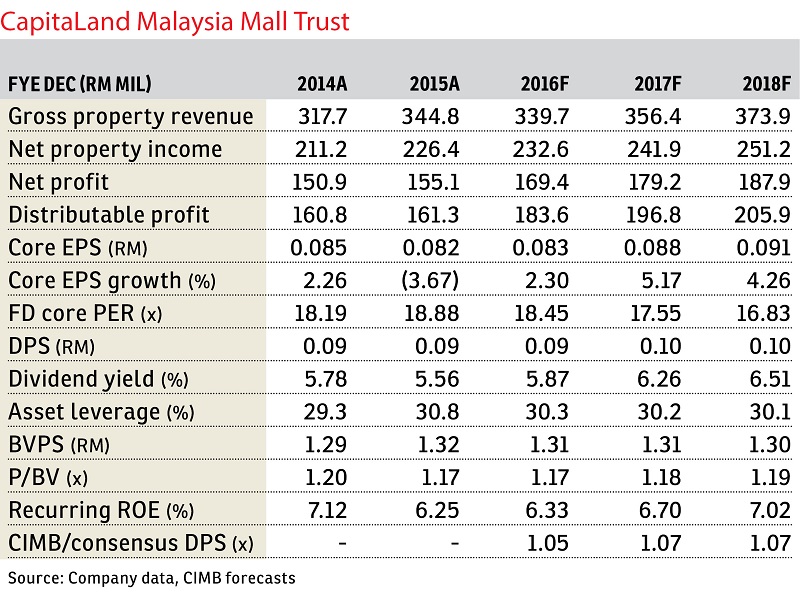

In the third quarter of 2016 (3Q16), CMMT’s top line rose 2.8% year-on-year (y-o-y) to RM93.5 million and bottom line increased 4.4% y-o-y to RM41.5 million. This brought its cumulative nine-month 2016 (9M16) core net profit to RM122.6 million, making up 72% of our full-year forecast and 71% of consensus. We expect a better fourth quarter given the additional contribution from Tropicana City Mall and Gurney Plaza (GP) malls, following the completion of its asset enhancement initiatives.

CMMT declared distribution per unit (DPU) of 2.13 sen for 3Q16, bringing its 9M16 DPU to 6.33 sen. We believe that the group is on track to meet our full-year DPU forecast of 8.6 sen.

In relation to 9M15, CMMT’s 9M16 revenue and core net profit growth was mainly underscored by the contribution from Tropicana City Property (TCP) as well as aided by the better showing from its East Coast Mall (ECM) and GP malls, which registered rental reversion of 11.5% y-o-y and 5.7% y-o-y respectively.

Stripping out the net property income (NPI) contribution from TCP, CMMT recorded flat 9M16 NPI growth. This was mainly due to the weakness in SWP and marginal decline from The Mines Shopping Mall, which saw NPI falling 26.3% and 0.8% y-o-y to RM21.2 million and RM38.7 million respectively. The 9M16 NPI growth of its ECM (+7.3% y-o-y) and GP (+9.5% y-o-y) malls was not enough to offset the NPI decline of SWP and The Mines.

Excluding SWP and TCP, CMMT’s average rental reversion rate rose 5.3% y-o-y for 9M16 as all its other properties posted positive rental reversions.

The impact of negative rental reversions of SWP (-37.9% y-o-y) and TCP (-6.7% y-o-y) in 9M16 was mitigated by its other properties such as ECM, GP and The Mines (+5.1% y-o-y), bringing overall 9M16 rental reversion rate to a softer decline of 1% y-o-y. — CIMB Research, Oct 21

This article first appeared in The Edge Financial Daily, on Oct 25, 2016. Subscribe to The Edge Financial Daily here.

TOP PICKS BY EDGEPROP

Taman Shanghai

Jalan Klang Lama (Old Klang Road), Kuala Lumpur

Aurora Residence @ Lake Side City

Puchong, Selangor

Amber Residence @ twentyfive.7

Kota Kemuning, Selangor

Amber Residence @ twentyfive.7

Kota Kemuning, Selangor

Amber Residence @ twentyfive.7

Kota Kemuning, Selangor

Amber Residence @ twentyfive.7

Kota Kemuning, Selangor

Amber Residence @ twentyfive.7

Kota Kemuning, Selangor

Taman Sri Putra, Sungai Buloh

Sungai Buloh, Selangor

Medan Idaman Business Centre

Setapak, Kuala Lumpur

HiCom-Glenmarie Industrial Park

Shah Alam, Selangor

{kind=link}