Protasco Bhd (Oct 20, RM1.15)

Initiate add recommendation with a target price (TP) of RM1.43: Protasco Bhd is the biggest play on government road maintenance contracts, with a dominant 43% market share in the road maintenance space last year (our estimates).

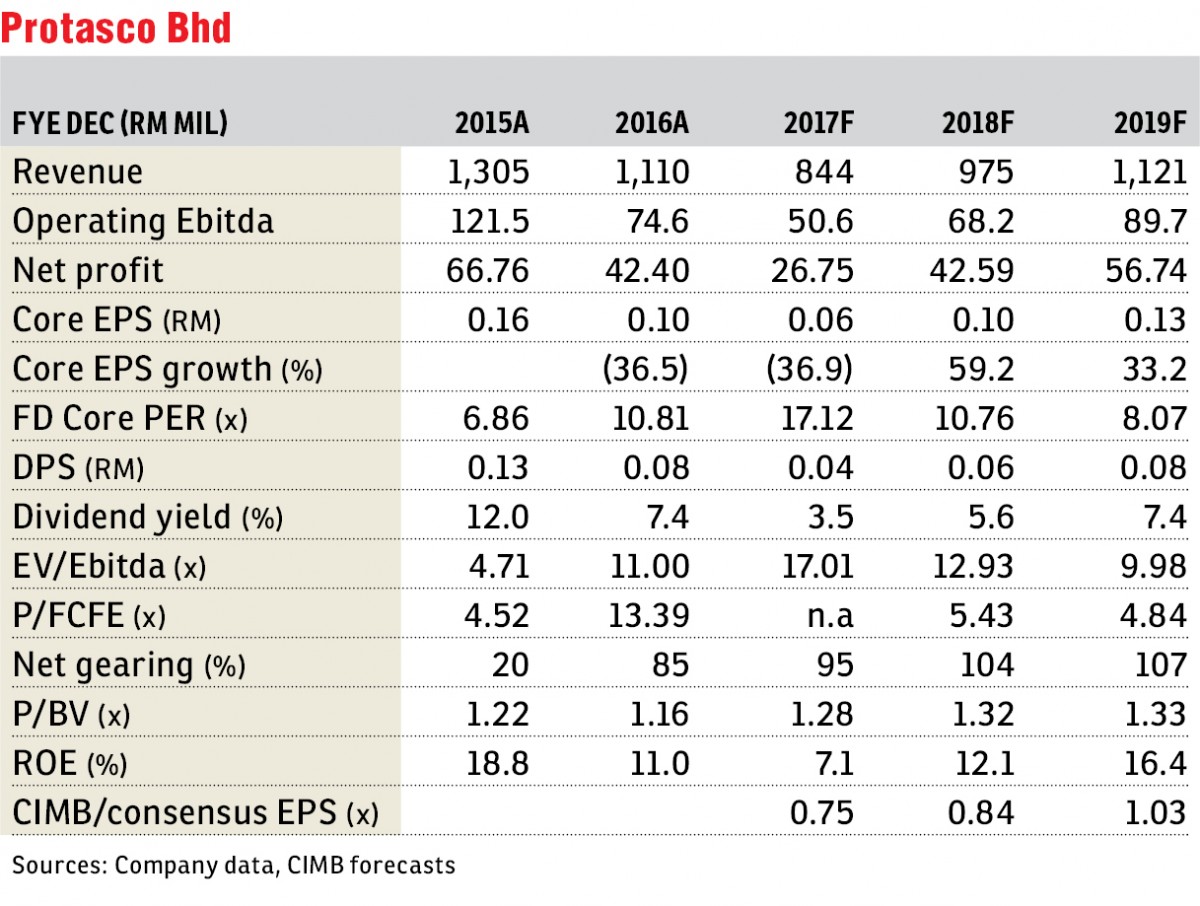

It is the only listed company with direct exposure to this segment and stands to benefit from an uptrend in government expenditure on road construction and maintenance (up more than 200% in the forecast for 2017 [2017F] to RM5.9 billion). Its construction division is vying for RM4.6 billion in new contracts, typically rolled out prior to the general election. We think its earnings will recover in financial year 2018 (FY18).

We consider the FY16 and FY17F transition years for Protasco’s earnings prior to contributions from road maintenance and construction stepping up to reflect higher-margin recurring earnings from a RM4.2 billion outstanding order book for road maintenance and billings for its high RM718 million construction order book. We forecast earnings recovery from FY18 to FY19, with a three-year earnings per share compound annual growth rate of 10% (FY16-FY19F).

Its current share price is 19% lower than the previous high in 2016 and at a massive 55% discount to the end of FY18F revalued net asset value (RNAV). We believe most of the negatives (disappointing FY16 results, likely sustained weak earnings in FY17F and legacy issues) are reflected in the current share price. The stock could be catalysed by: i) a revival in contract flows, ii) election plays, and iii) revival in affordable housing contracts (Protasco’s niche area).

Protasco’s dividend appeal is supported by stable earnings from its road maintenance concessions. We forecast a dividend payout ratio of 60% in the FY17-FY19F (consistent with historical ratios) period and exclude potential special dividends. Its FY18-FY19F dividend yields of 6%-7% (our estimates) are the highest in the sector and among the small-cap contractors.

Protasco’s current share price implies that investors would essentially be paying for only its road maintenance division (which accounts for 44% of our end of the FY18F RNAV per share of RM2.39) and getting other assets for “free”.

Construction, property development, trading/manufacturing and education make up the balance 54% of RNAV. Year to date, Protasco’s share price has marginally increased by 0.7%, compared to the stellar 14%-100% rerating of comparable small-cap contractors.

We believe Protasco offers an attractive risk-reward profile from FY17 to FY18F. Initiate with add and a RM1.43 TP, based on a 40% discount to the end of FY18F RNAV (implied end of 2018F target price-earnings ratio [PER] of 14.3 times). At 8-11 times the 2018-19F PER, Protasco trades at a 14%-18% discount to the PER valuations of selected small/mid-cap contractors. Key downside risks to our call are weak earnings delivery, poor execution and job delays. — CIMB Research, Oct 19

This article first appeared in The Edge Financial Daily, on Oct 23, 2017.

For more stories, download EdgeProp.my pullout here for free.

TOP PICKS BY EDGEPROP

Kenny Hills (Bukit Tunku)

Kenny Hills (Bukit Tunku), Kuala Lumpur

Avantro Residences @ Bandar Kinrara

Puchong, Selangor

Bandar Seri Coalfields

Sungai Buloh, Selangor

Avantro Residences @ Bandar Kinrara

Puchong, Selangor

Bandar Damai Perdana

Bandar Damai Perdana, Selangor

Megan Phoenix Business Centre

Cheras, Kuala Lumpur

Seksyen 1, Petaling Jaya

Petaling Jaya, Selangor

{kind=link}