- How do we compare our building costs to those in neighbouring countries? Are Malaysian developers making excessive profits? Are they building the wrong products at unreasonably high prices to maximise profits, resulting in an excessive number of unsold houses, instead of building more affordable houses?

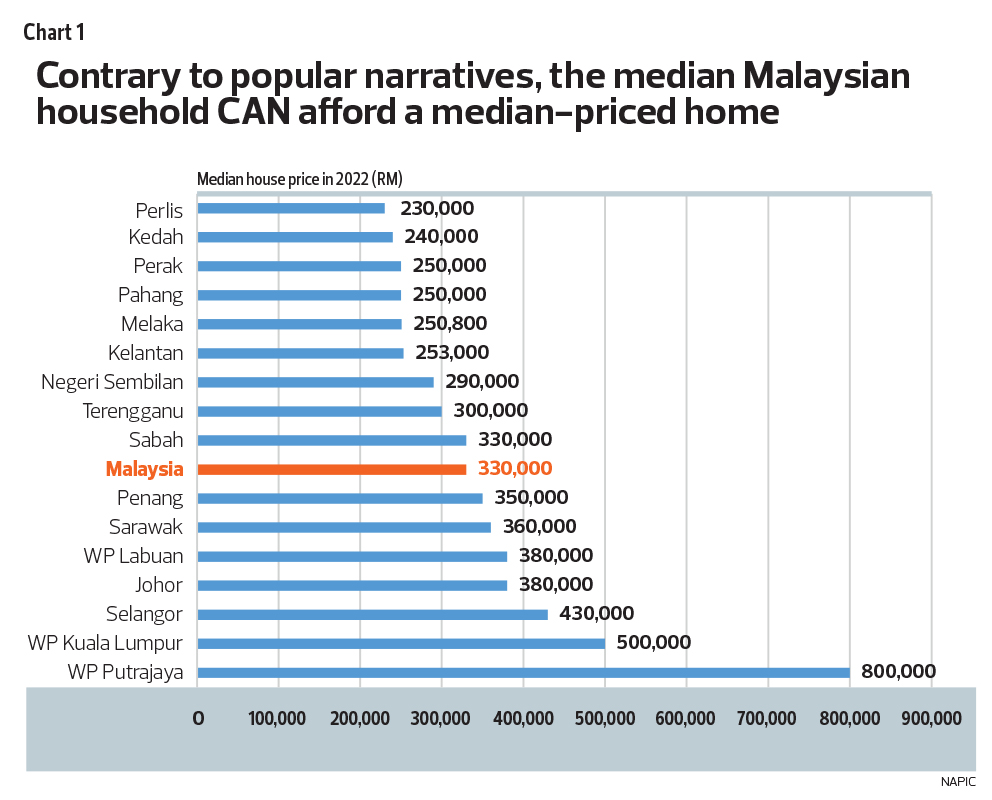

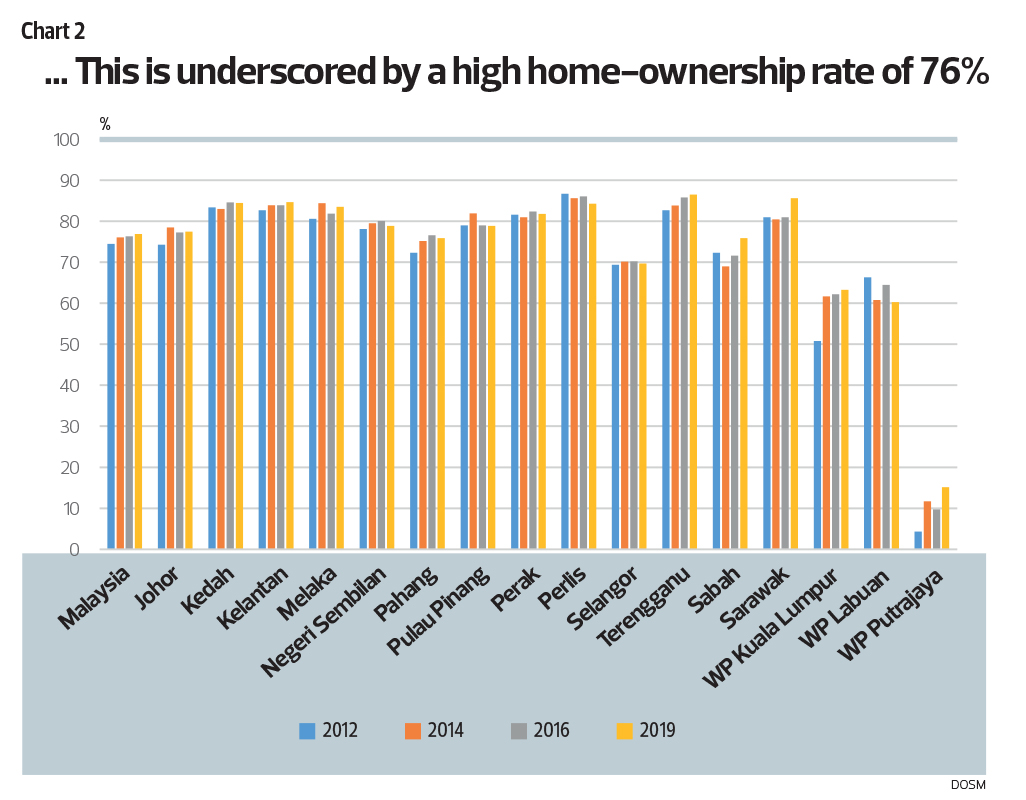

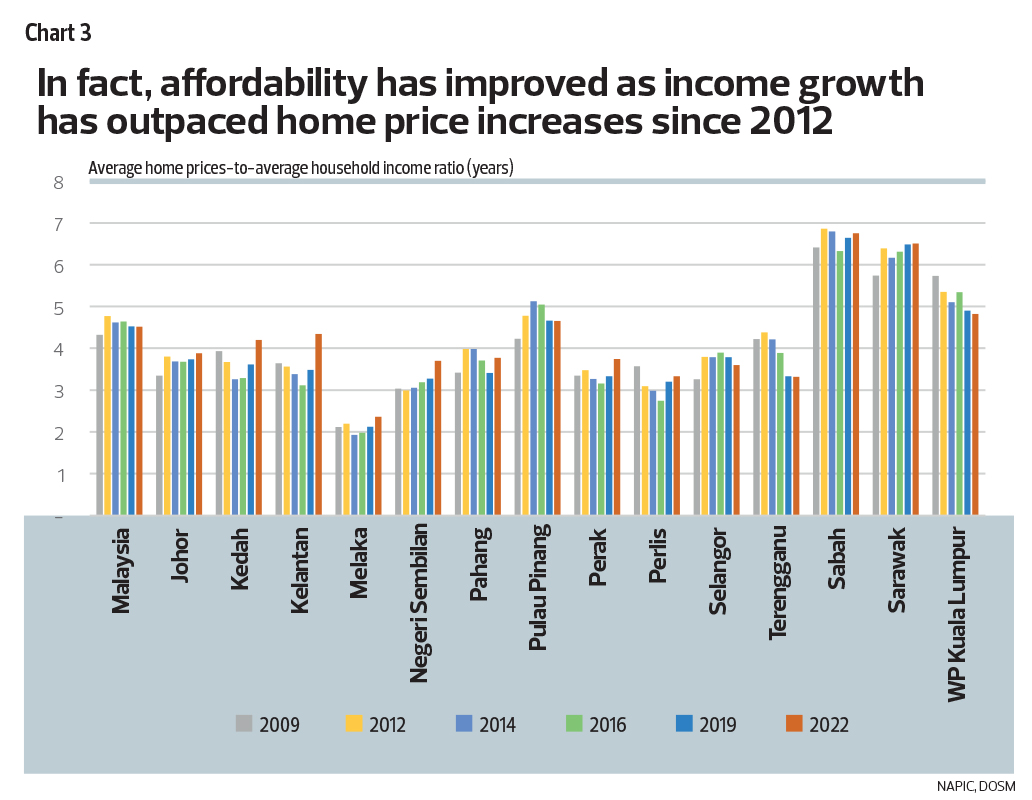

Last week, we provided our data-based analysis that contradicts the prevailing myth that housing is generally unaffordable in Malaysia. At the prevailing median household income of RM5,209 a month, and allowing 50% of disposable income (of RM4,543 a month) to be spent on fixed commitments (home mortgages and instalments on car loans), it translates into a median affordable house price of RM350,000, higher than the RM330,000 median house price for all of Malaysia in 2022, according to the National Property Information Centre (Napic) (see Chart 1). This conforms to the fact that the home ownership rate has gradually risen since 2012 and is now about 76% (see Chart 2). The reason is that the ratio of average home price to average household income has gradually fallen since 2012 (that is, income rose faster than house prices) (see Chart 3).

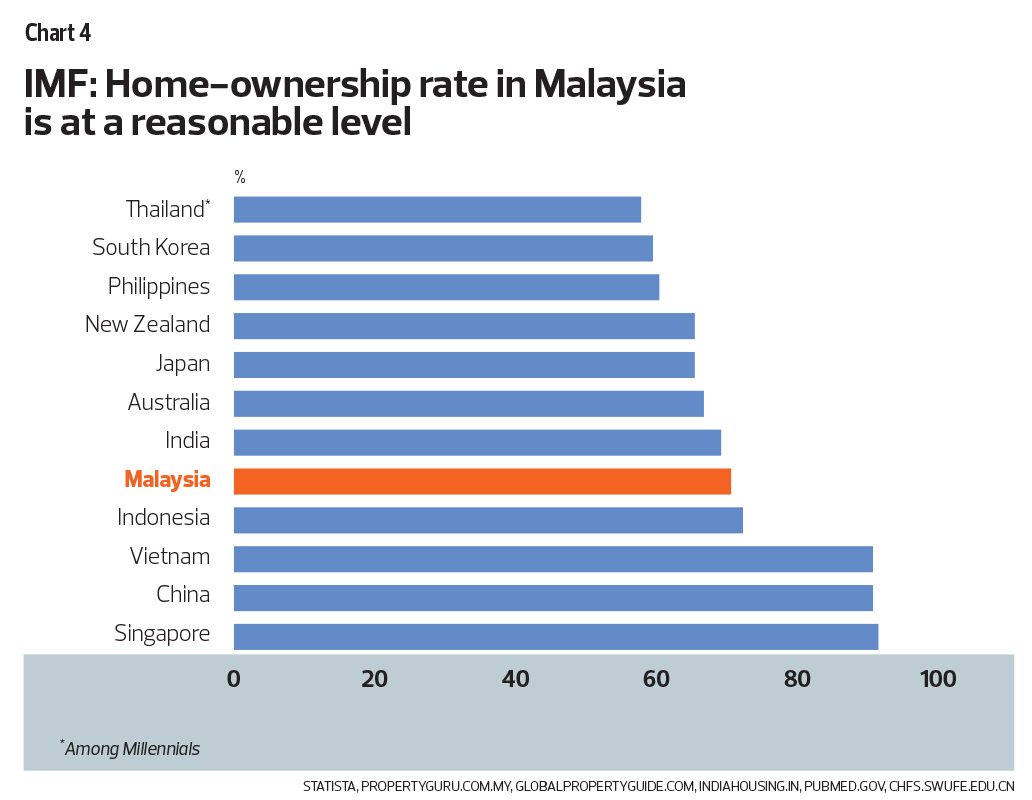

This conclusion is consistent with statistics from the International Monetary Fund (IMF) (in its paper entitled “Housing Stability and Affordability in Asia-Pacific”) that the home ownership rate in Malaysia is at a reasonable level, although behind that of Singapore, China and Vietnam (each of which has strong unique reasons) (see Chart 4).

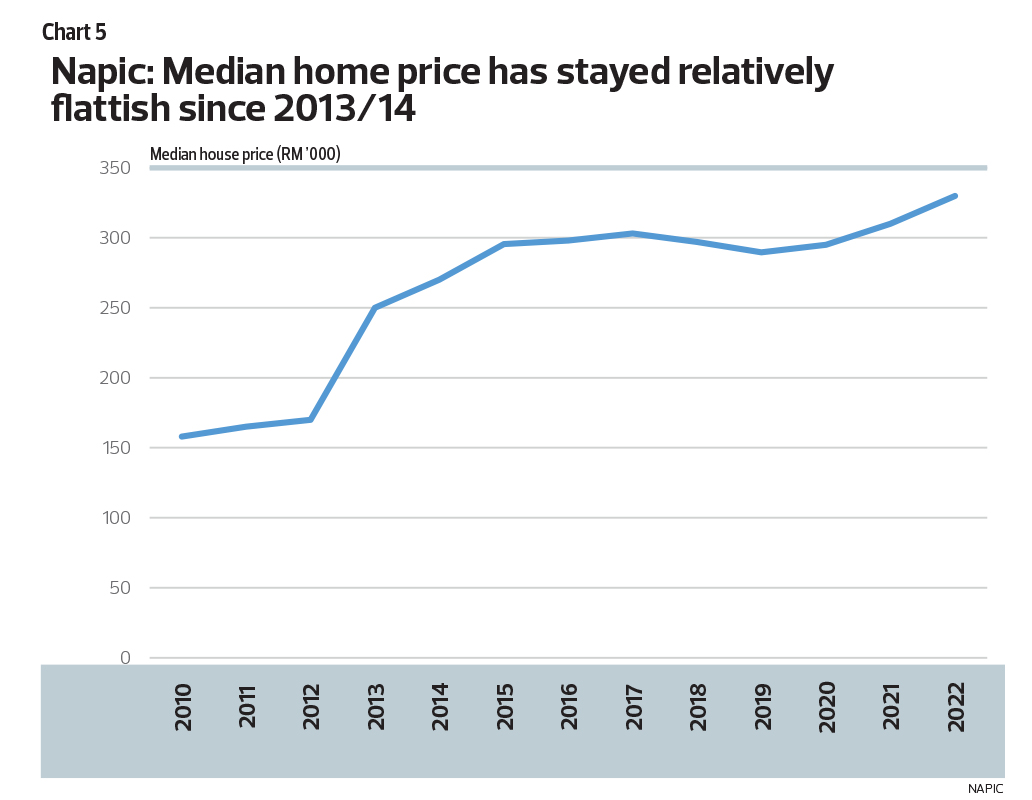

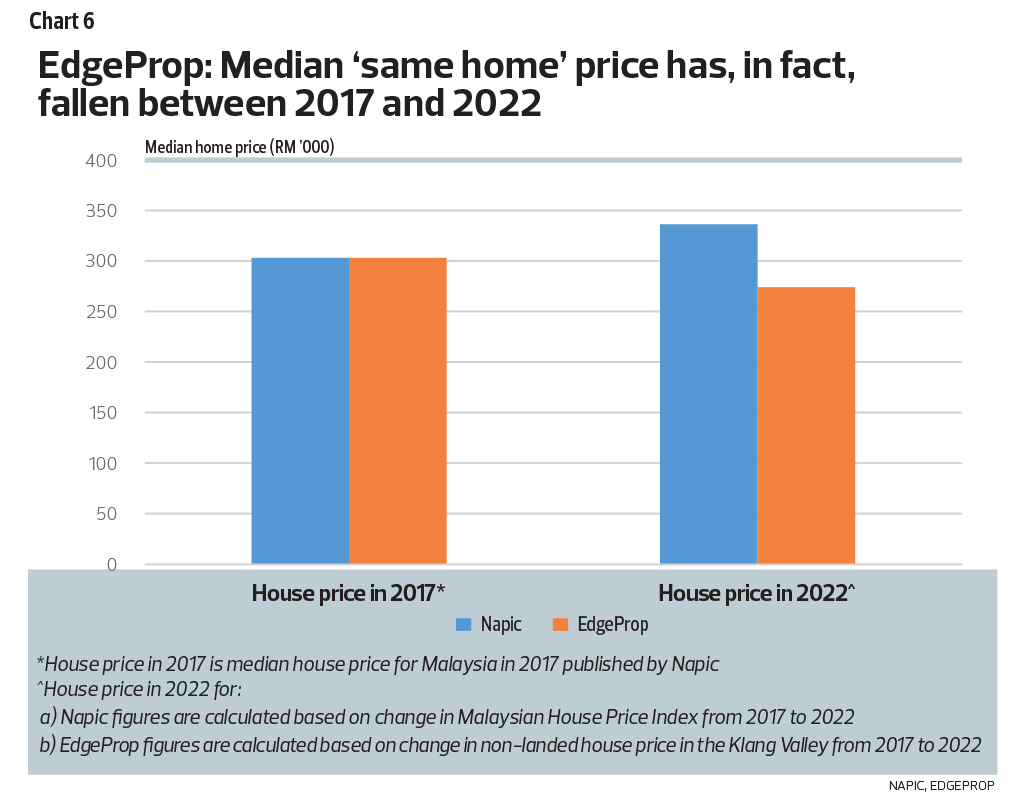

The Napic data for median house prices since 2010 (Chart 5) shows that house prices in Malaysia have stayed flattish since 2013/14. And last week, we articulated why house prices shot up from 2009 to 2013, owing to speculation arising from the introduction of the Developer Interest Bearing Scheme (DIBS), which was abolished in 2014. Again, as we articulated last week, even this flattish median house price data from Napic is an overestimation of the increase in house prices in Malaysia, in our view. As shown in Chart 6, our own data from EdgeProp using “same house” showed an actual decline in the median home price from 2017 to 2022.

Do we then conclude that Malaysia has an efficient and competitive home building industry and ecosystem? Could homes be built at even lower costs to further improve affordability? How do we compare our building costs to those in neighbouring countries? Are Malaysian developers making excessive profits? Are they building the wrong products at unreasonably high prices to maximise profits, resulting in an excessive number of unsold houses, instead of building more affordable houses?

What can we do to assist those who need social and subsidised housing, or low-cost housing, owing to unemployment, health issues or simply earning very low wages? As we articulated last week, housing is a human right that requires public sector intervention.

This week, we articulate our views on the above difficult questions. We do not pretend to know all the answers and neither do we insist we are necessarily right. But we do believe that laying out the facts and articulating different viewpoints are necessary to arrive at reasonable conclusions and decisions.

Question 1: Is the Malaysian housing industry efficient and competitive?

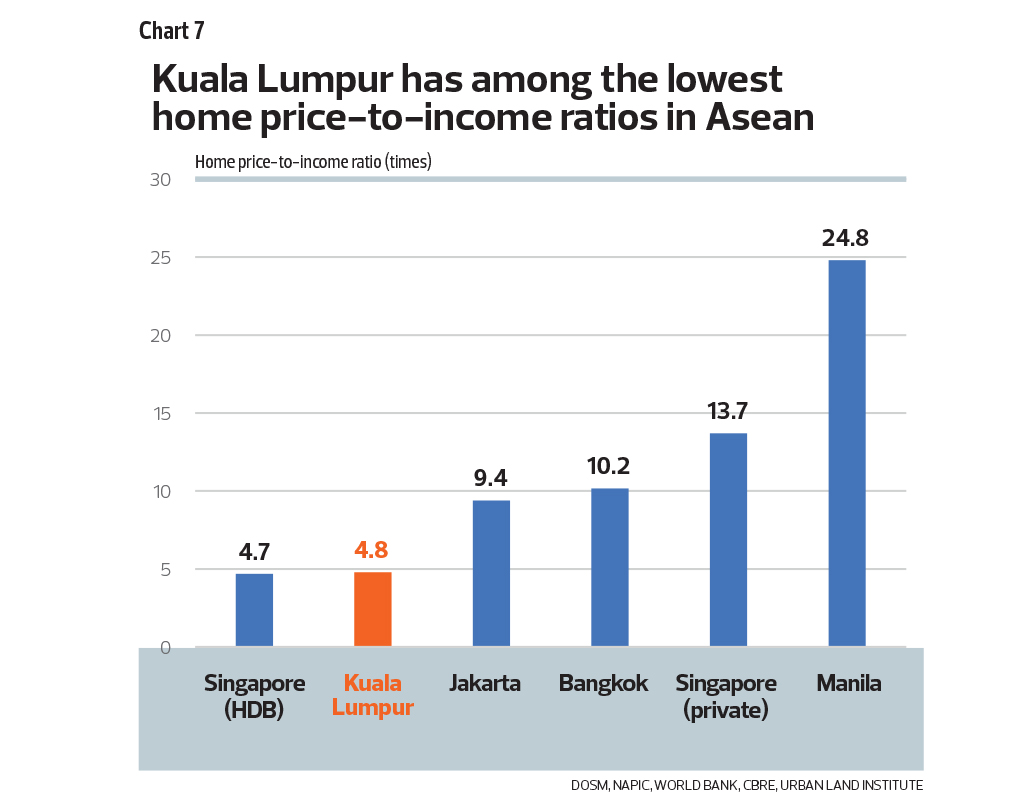

Chart 7 shows the median house price-to-median household income in five major Asean cities — Kuala Lumpur has the lowest ratio, after Singapore. This means that affordability is very high in Kuala Lumpur, comparable to Singapore HDB housing.

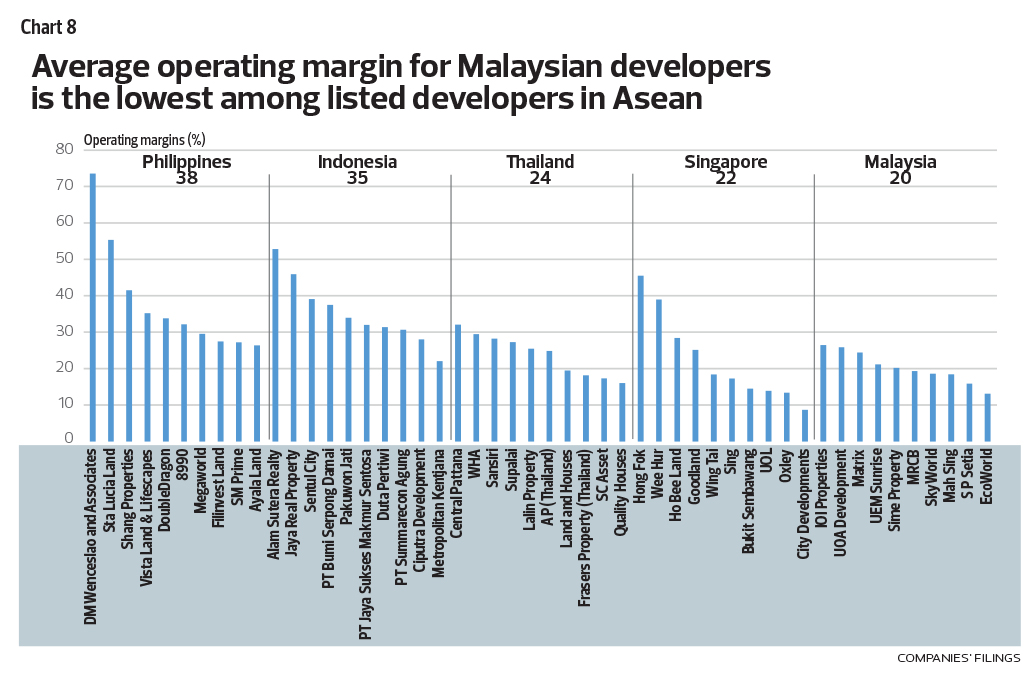

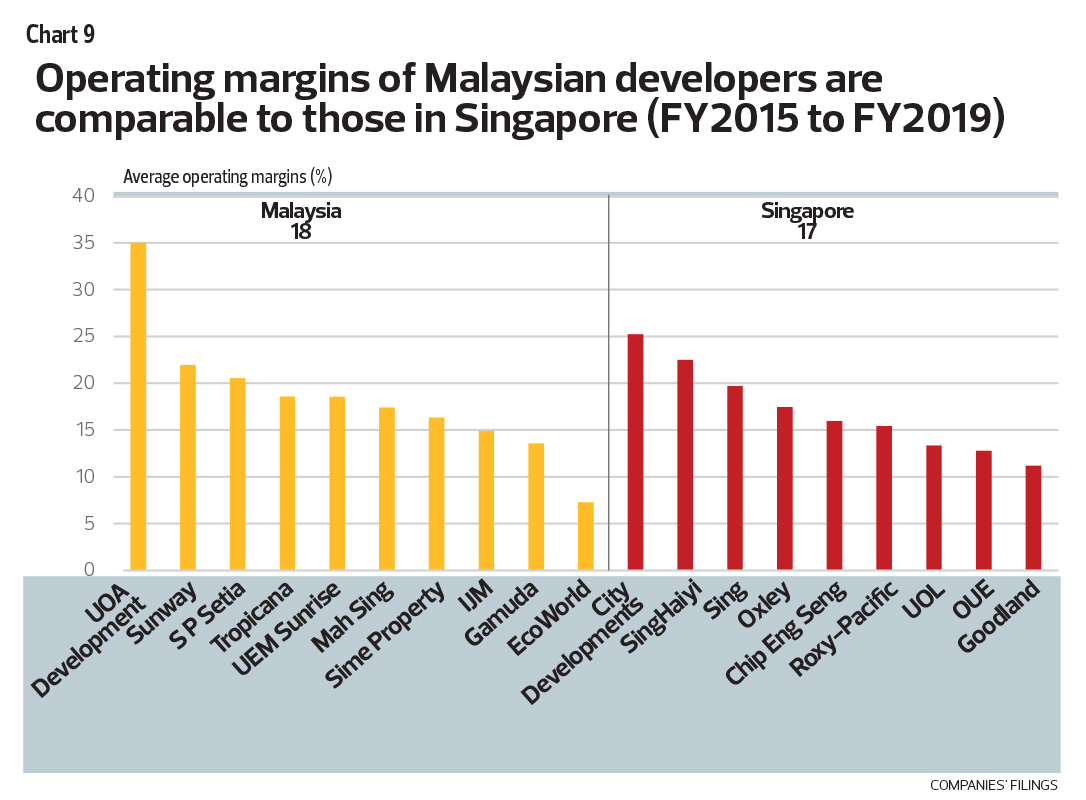

The next question is, at the selling prices, do Malaysian developers make excessive profits (operating margins)? Chart 8 shows the operating margins of Malaysian-listed property developers averaging at 20% for the latest financial year. This is the lowest among listed developers in Asean, comparable to Singapore. This result is then time-tested against the financial results for 2015 to 2019 (see Chart 9).

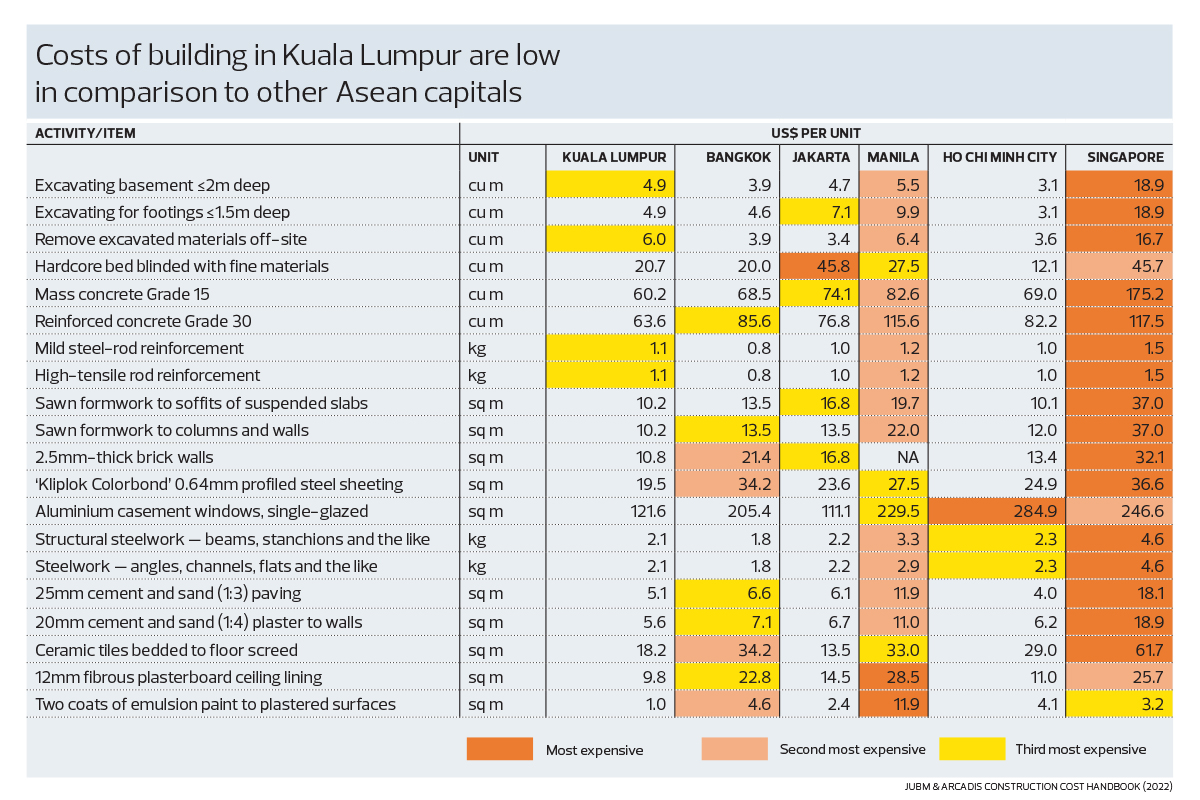

The above conclusions are consistent with the fact that the costs of building in Kuala Lumpur are low in comparison to other Asean capitals (see table). As expected, Singapore has the highest construction costs.

Therefore, the logical conclusion is that the property development and construction industry in Malaysia is efficient and competitive. It is certainly not less competitive and efficient than in any of the other Asean countries. Construction costs are low and profit margins are highly competitive, thereby enabling houses to be sold efficiently to meet the demand of homeowners.

Question 2: Are Malaysian developers building the wrong products, resulting in high unsold inventories (of high-priced units) while not meeting the demand in the market for lower-priced houses?

This is an oft-quoted narrative of those who demand greater government intervention. Developers are greedy and build high-priced houses to maximise profits. Theoretically, this argument makes no sense. There is no profit if you cannot sell. Indeed, losses will be substantial, since profit margins are 20% or less. But let us look at the facts.

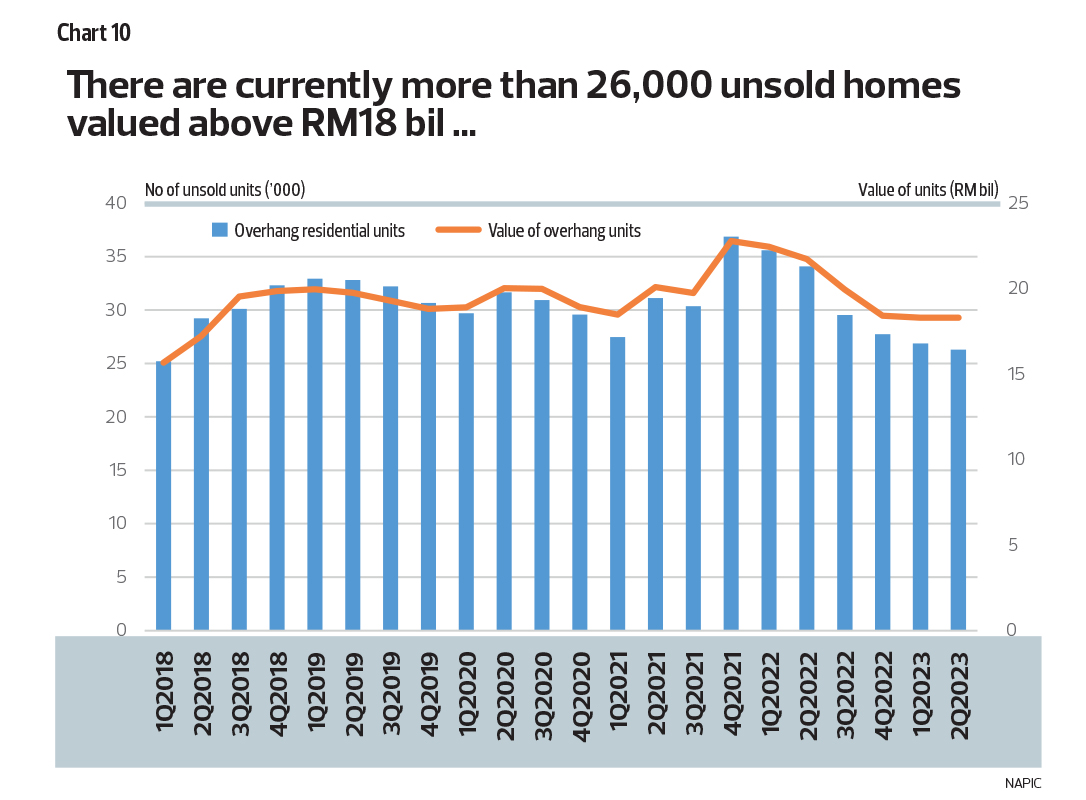

Chart 10 shows Napic data on unsold units and the value of these unsold units in Malaysia. The number of unsold units reached a peak of 37,000, valued at RM22.8 billion in 2021. The current number of unsold units is more than 26,000, valued at more than RM18 billion. These astonishingly high numbers are the reason that many see unsold units as a key challenge for the property industry, concluding that developers are not building what the market needs.

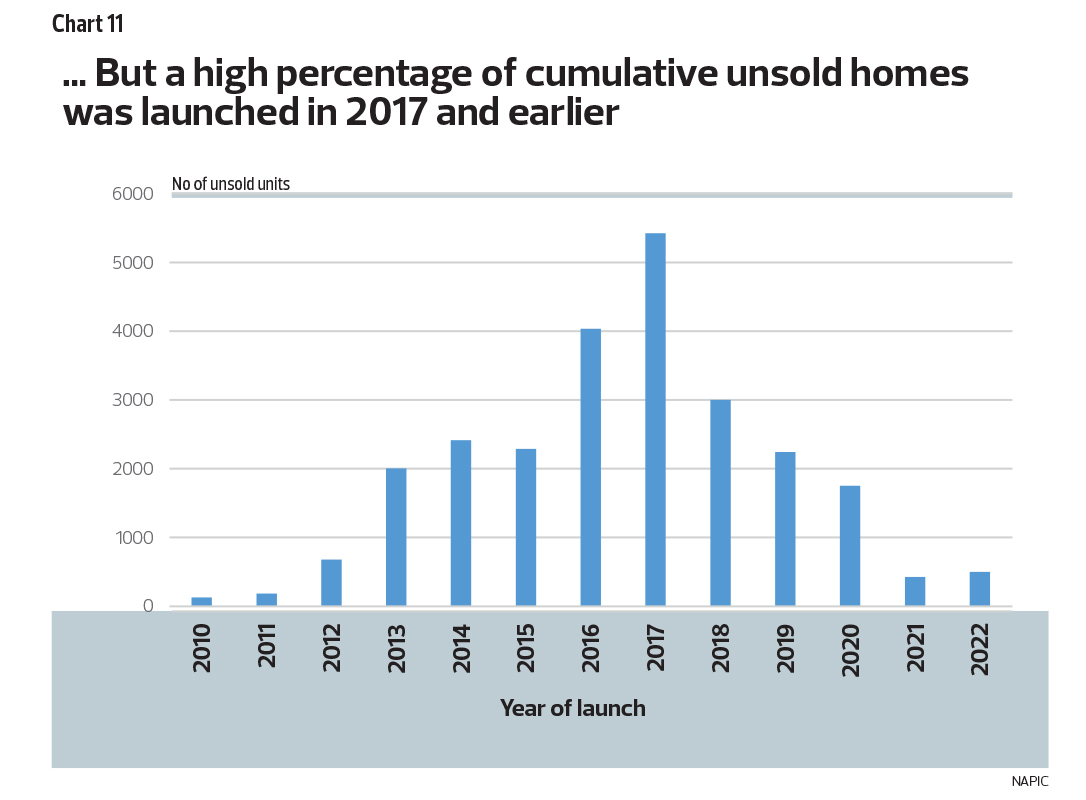

Looking at the time series of this data, the number of unsold units has consistently exceeded 25,000, with a value of more than RM15 billion. A closer scrutiny of the unsold units shows that most were launched in 2017 and earlier, that is, launched more than six years ago and completed more than three years ago (see Chart 11). The question is whether many of these “unsold” units should still be counted. They were obviously “mistakes”, whether it is bad location, badly built, badly priced or, for a host of others reasons, could not be sold. Removing this base of 25,000 units will result in a very different conclusion.

Surely we must conclude that Napic’s reported number of unsold houses is in fact exaggerated. If so, then the actual number of unsold houses is not a significant challenge except in specific locations and for specific reasons, such as Country Garden’s Forest City in Johor. As in all production, there is inevitable wastage and spoilage that must be written off and scrapped. Nothing is achieved by recording it in inventory as unsold.

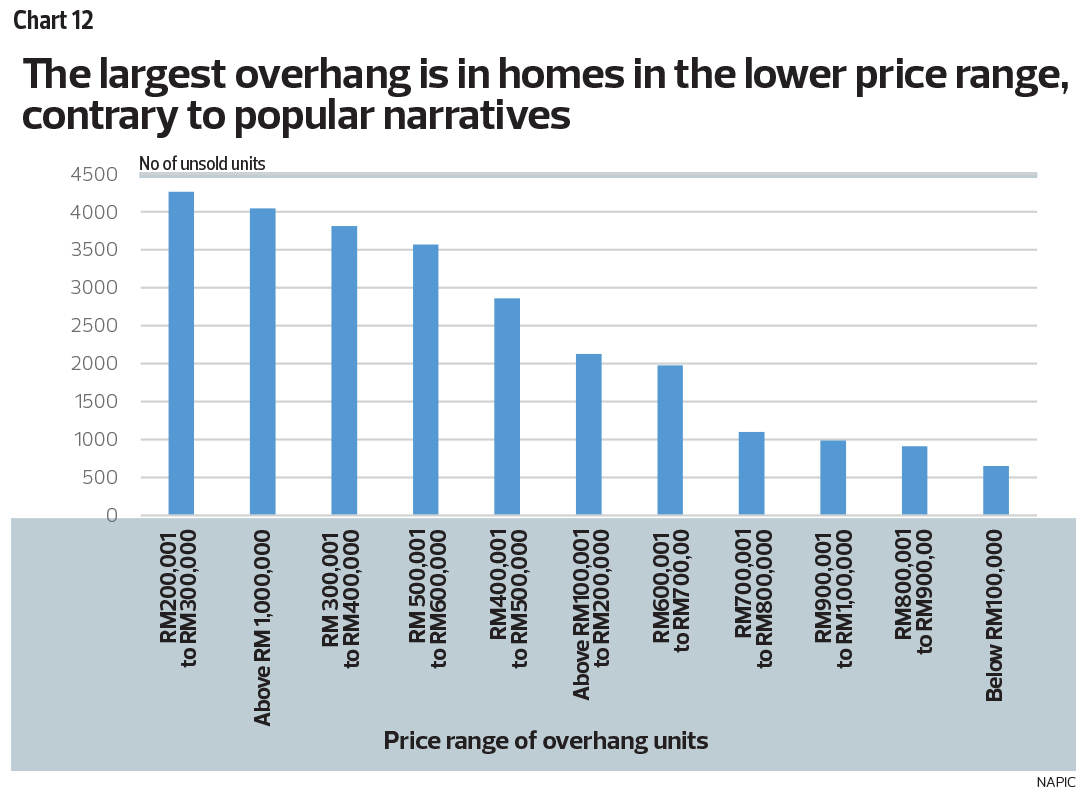

Chart 12 shows the number of unsold units by price range. The largest number of unsold units is priced at the lower price range. Indeed, the lower the price, the larger the number of unsold units. This contradicts the narrative that the high number of unsold units is because developers are building higher-priced products that cannot be sold because of unaffordability.

Question 3: How can we address the needs of social or subsidised housing (sometimes referred to as public or low-cost) for those who cannot afford houses built commercially by the private sector?

We define social or subsidised housing as meeting the needs of those who cannot compete in the market or afford to be homeowners or rent decent housing in the private market. They are generally the vulnerable and poor, the elderly and some first-time young buyers. Social housing is therefore supplied at prices that are lower than the general housing market and is distributed by administrative procedures. This means that governments are inevitably involved.

All countries face this challenge; how they cope differs. Solutions include social rented housing, low-cost home ownership (either the state or state with the private sector provides subsidised housing for sale), cooperatives (pooling members’ resources), shared ownership or fractional ownership (paying rents on the fraction they do not own) or the government providing funding and financing for social housing to reduce either construction costs (supply-side subsidies) or rentals (demand-side subsidies).

Financing is a key challenge to ownership and there are various instruments available, including subsidies for first-time home buyers, preferential interest rates, early withdrawal from provident funds, government guarantees or loans, and tax deductibility for mortgage interest.

Eligibility also differs across countries. Some financing is available for a wide range of income levels; others are below a certain income threshold; and yet others are only for a very defined population (such as only vulnerable and special groups). This is often dependent on the political considerations and budgetary constraints of each government.

The most common way to provide social housing is for developers to reduce their costs — often by relaxing regulations; providing cheap land or higher plot ratios in return; offering tax credits or tax benefits; or government supported sources of cheap long-term funding — and profits as a trade-off and social contribution. This prevents the government from being directly involved in the building of this low-cost housing and all its pitfalls.

The point we are making is that we must have clarity on the issues and challenges. What exactly do we want to address? We have established that housing in general in Malaysia is not unaffordable. We have established that the property industry and ecosystem are efficient and competitive. We have established that the actual meaningful unsold units are not excessive (besides specific locations and projects that are best addressed with specific measures), property prices in Malaysia are fair, and our construction is efficient, and costs are low and competitive.

The real challenge is in fact the need for social or subsidised or low-cost housing for those eligible (and we need to first define who these Malaysians are). The solution should therefore be focused on this specific challenge and not be diverted to all sorts of government interventions to regulate and intervene in the private housing market, which is already efficient and competitive. As we explained earlier, this is a challenge literally every country in the world must deal with. And there are many different and similar measures already in place, including in Malaysia.

We refer readers to a couple of well-articulated literature and research on this topic: a report commissioned by Shelter and carried out by URBED Trust entitled “Learning from international examples of affordable housing” dated July 2018; and an OECD 2020 report entitled “Social housing: A key part of past and future housing policy”.

For Malaysia, we suspect the optimal solution is likely to be one without direct government building or paying or guaranteeing social housing, given past failures such as PR1MA and the inevitable leakages. We think social housing should be landed and not high-rise, since the land value component will rise over time to create savings and wealth (lack of social-consciousness and affordability will inevitably lead to degradation for strata-type properties). The government can reduce the costs to make these developments profitable for private developers to undertake by providing cheap land and infrastructure (especially transport connectivity) as well as cheap long-term capital or financing and tax incentives (supply-side incentives).

The current system in which private developers are forced to subsidise by building and selling affordable houses — as part of their total development — below cost is inefficient. It simply adds higher costs to all homes for sale, as developers must recoup this subsidy. A better approach is to have transparency and clarity on making sure the industry is competitive and efficient, producing homes that buyers demand at the lowest costs, and, separately, dealing with the specific needs of social housing.

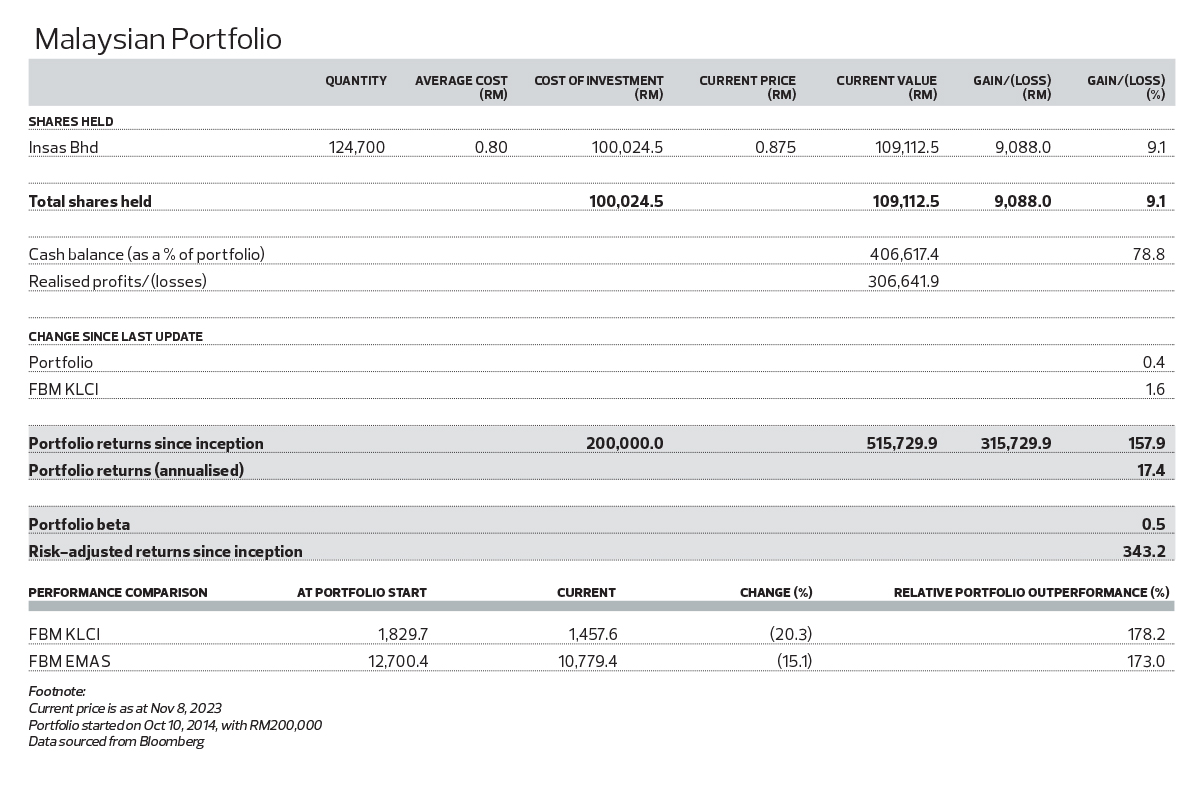

The share price of Insas, our only stock holding, gained 1.7% last week. Owing to our high cash balance, however, the Malaysian Portfolio was up by only 0.4%. Total portfolio returns now stand at 157.9% since inception. The portfolio is outperforming the benchmark FBM KLCI, which is down 20.3%, by a long, long way.

Disclaimer: This is a personal portfolio for information purposes only and does not constitute a recommendation or solicitation or expression of views to influence readers to buy/sell stocks. Our shareholders, directors and employees may have positions in or may be materially interested in any of the stocks. We may also have or have had dealings with or may provide or have provided content services to the companies mentioned in the reports.

Looking to buy a home? Sign up for EdgeProp START and get exclusive rewards and vouchers for ANY home purchase in Malaysia (primary or subsale)!

TOP PICKS BY EDGEPROP

Apartment Tanjung Puteri Resort

Pasir Gudang, Johor

Seri Mutiara Apartment, Bandar Baru Seri Alam

Masai, Johor

{kind=link}