Hock Seng Lee Bhd (Aug 17, RM1.45)

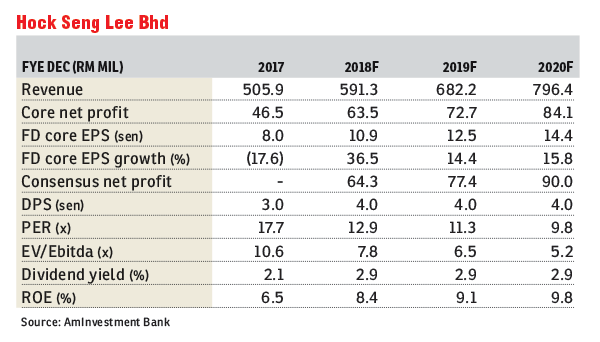

Maintain hold with a fair value of RM1.25: We maintain our forecasts, “hold” call, and fair value (FV) of RM1.25 based on 10 times financial year 2019 (FY19) earnings per share (EPS), in line with our benchmark forward target price-earnings ratio of seven to 10 times for small-cap construction stocks.

Hock Seng Lee Bhd’s (HSL) net profit for first half of financial year 2018 (1HFY18) came in at only 44% and 43% of our and consensus full-year forecasts respectively. However, we consider the results within expectations as we expect stronger quarters ahead with key construction projects gathering momentum.

At present, the progress of these key projects stands at: i) 30% for the RM1.2 billion work package for the Pan Borneo Highway (total value for the work package is RM1.7 billion, HSL has a 70% share); ii) 18% for the RM333 million Miri Wastewater Management System; and iii) 5% for the RM563 million Kuching City Central Wastewater Management System (Phase 2) (total contract value is RM750 million, HSL has a 75% share). Collectively, these three jobs make up two-thirds of HSL’s outstanding construction order book of RM2.5 billion. Our forecasts assume job wins of RM250 million annually FY18 and FY20. So far in FY18, HSL has only secured one key contract worth RM101.2 million for the construction of Maktab Rendah Sains Mara in Bintulu, Sarawak.

1HFY18 net profit grew by a third year-on-year (y-o-y) thanks largely to stronger construction profit as the three key projects started to contribute more significantly, coupled with a slight improvement in property profit.

We remain cautious about the outlook for the local construction sector. As local contractors compete for a shrinking pool of new jobs in the market, they tend to undercut each other, resulting in razor-thin margins for the successful bidders. On the other hand, the introduction of a more transparent public procurement system under the new administration should weed out rent seekers, paving the way towards healthier competition within the local construction sector.

We believe HSL will be able to ride out the current downturn in the local construction sector relatively better than its peers, given its substantial order backlog that should keep it busy over the next three to four years, coupled with its ability to compete under an open bidding system. — AmInvestment Bank, Aug 16

This article first appeared in The Edge Financial Daily, on Aug 20, 2018.

For more stories, download EdgeProp.my pullout here for free.

TOP PICKS BY EDGEPROP

Menara Bintang Goldhill

Bukit Bintang, Kuala Lumpur

Kawasan Perindustrian Batu Caves

Batu Caves, Selangor

Kawasan Perindustrian Meru Timur

Klang, Selangor

Arab Malaysian Industrial Park

Nilai, Negeri Sembilan

Arab Malaysian Industrial Park

Nilai, Negeri Sembilan

Menara Bintang Goldhill

Bukit Bintang, Kuala Lumpur

Taman Perindustrian Kapar Bestari

Kapar, Selangor

The Sky Residence @ Shamelin

Cheras, Kuala Lumpur

{kind=link}