Real estate investment trust sector

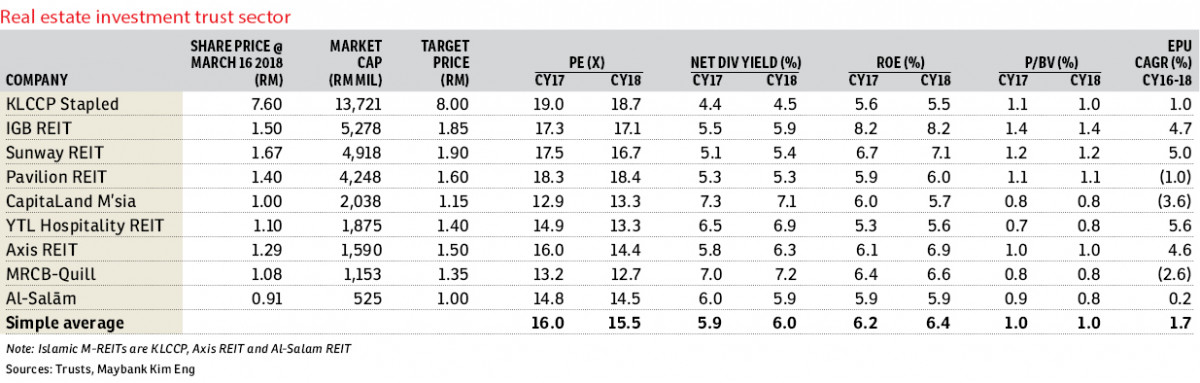

Maintain neutral: We are mildly positive on the revised Guidelines on Real Estate Investment Trusts (REITs) which allow property development for Malaysian REITs (M-REITs), among other changes/additions. This new property development ruling is within our expectations and it could benefit selected M-REITs. We remain “neutral” on the sector and our selective buys are IGBREIT, SunREIT, CMMT, YTLREIT and MQREIT.

The Securities Commission Malaysia (SC) has released the revised Guidelines on REITs (including non-listed REITs) on March 15, 2018, which takes effect on April 9, 2018 (previous version was released on Dec 28, 2012). As anticipated, the revised guidelines now allow M-REITs to undertake property development activities (including acquisition of vacant land). We are slightly positive on this new ruling as it would enable M-REITs to increase their earnings and yields via asset development/redevelopment activities. However, we believe this would only benefit M-REITs with medium to large asset value bases due to limitations on their aggregate investment value (from development activities) up to 15% of the M-REIT’s total asset value.

Elsewhere, we think selected revisions such as the fixed borrowing limit (50% of total asset value) and requirement to revalue assets at least once per financial year will enhance unitholder value. However, M-REITs would incur some additional non-operating expenses on asset revaluations.

The revised guidelines also incorporated and expanded on the Islamic REIT rulings, which supersede the current standalone Guidelines for Islamic REITs (released on Nov 21, 2005). We are generally positive on the revision as it contains a wider scope for Islamic REITs rulings and relaxes the ruling on syariah non-compliant tenants. This would be beneficial to Islamic REITs with retail malls such as Suria KLCC by KLCCP and Komtar JBCC by ALSREIT.

We maintain our assumptions and forecasts on M-REITs and remain “neutral” on the sector. The broad sector outlook remains challenging due to the oversupply of office space and retail malls, especially in the Klang Valley. That said, we remain selectively positive on M-REITs with prime office assets and malls with long-term tenants where their earnings will be driven by sustained occupancy rates and positive rental reversions. Our top retail “buy” pick is IGBREIT, backed by its two prime malls’ prominent locations and active footfall-driving activities which would entail continuous high demand for its retail space. — Maybank Research, March 19

This article first appeared in The Edge Financial Daily, on March 20, 2018.

For more stories, download EdgeProp.my pullout here for free.

TOP PICKS BY EDGEPROP

Ecohill Walk Mall, Setia Ecohill

Semenyih, Selangor

KSL Residence 2 @ Kangkar Tebrau

Johor Bahru, Johor

KSL Residence 2 @ Kangkar Tebrau

Johor Bahru, Johor

{kind=link}