S P Setia Bhd (Nov 10, RM3.29)

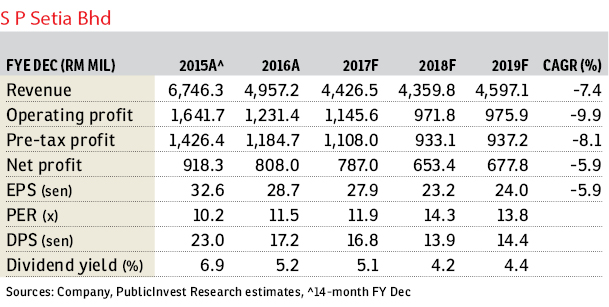

Maintain outperform with an unchanged target price (TP) of RM4.50: For the third quarter ended Sept 30, 2017 (3QFY17), S P Setia Bhd registered a net profit of RM253.2 million (+88.9% year-on-year [y-o-y]; +85.8% quarter-on-quarter), which was largely within our and consensus expectations.

Year to date (YTD), the group’s net profit of RM494.7 million (+29.1% y-o-y) only constituted about 63% and 66% of our and consensus full-year estimates, but we expect 4QFY17 results to continue to be strong, with the remaining billings from the Battersea Power Station and local projects.

Total unbilled sales remained healthy at RM7.05 billion, and we believe the group should be on track to meet its sales target of RM4 billion for FY17 (nine months of FY17 new sales: RM2.82 billion).

YTD new sales of RM2.82 billion came from local projects, which contributed RM1.66 billion (or 59% of total sales), and the remaining from international projects, which contributed RM1.16 billion.

Locally, new sales were largely from the central region with RM1.17 billion, whereas the southern and northern regions collectively sold RM495.6 million worth of property.

As for international projects, Sapphire by the Gardens in Melbourne was the key contributor, with a strong take-up rate of 83% amounting to RM871.7 million of the total of RM1.16 billion overseas sales secured by the group. We understand that the group has continued to see strong sales from overseas projects for FY17.

We understand that it will focus more on the launches of mid-range landed property in the Klang Valley in the near term.

Given current market conditions, the group has repositioned the launch of its condominium project, such as Setia Sky Seputeh (Tower B), while bringing forward the launches of more mid-priced landed property.

All in, projects worth about RM2.03 billion are expected to be unveiled in 4QFY17, which include new phases of Setia Alam, Setia EcoHill, Setia Eco Templer and KL Eco City.

This, in our view, demonstrates the group’s ability to change its product offerings based on market demand. This is only possible due to its vast land bank that enables the group to recalibrate its launches to suit property market conditions.

During the quarter, local billings were slower due to the transitional effect from selling more property from new townships, such as Setia Eco Templer and Setia EcoHill 2. This was mitigated by the substantial contribution from the Battersea Power Station.

All told, we maintain our “outperform” call, with an unchanged TP of RM4.50, pegged at an about 25% discount to revalued net asset value.

We still favour S P Setia for its sizeable and well located land bank, consistent performance, good earnings visibility and decent dividend yield. — PublicInvest Research, Nov 10

This article first appeared in The Edge Financial Daily, on Nov 13, 2017.

For more stories, download EdgeProp.my pullout here for free.

TOP PICKS BY EDGEPROP

Taman Bukit Indah @ Iskandar Puteri

Johor Bahru, Johor

Jalan Pasar Baru, Pekan Semenyih

Semenyih, Selangor

DC Residensi (Damansara City)

Damansara Heights, Kuala Lumpur

{kind=link}