Sunway REIT (Nov 1, RM1.73)

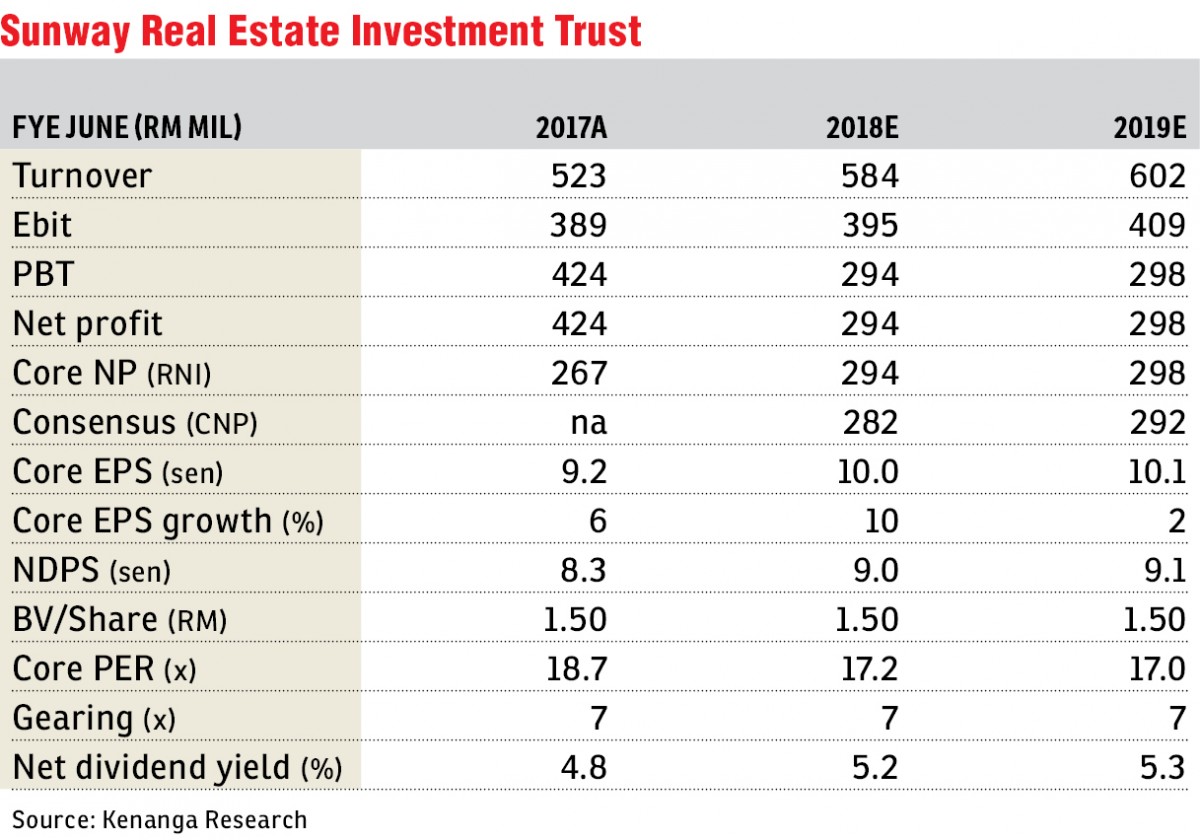

Maintain outperform rating with an unchanged target price (TP) of RM1.87 per share: First quarter of financial year 2018 (1QFY18) realised net income (RNI) of RM78.7 million came in within expectations, making up 28% and 27% of consensus and our estimates, respectively. 1QFY18 gross dividend per unit (GDPU) of 2.67 sen includes a non-taxable portion of 0.33 sen which is also within our expectations at 27% of estimated FY18E GDPU.

Year-on-year to year to date gross rental income (GRI) was up by 10% driven by all segments; (i) retail (+3.9%) on all assets from stable occupancy and positive reversions, save for SunCity Ipoh Hypermarket, (ii) hotel segment (+40.9%) driven by Sunway Pyramid Hotel post the completion of the refurbishment in June 2017, Sunway Putra Hotel benefiting from the SEA and Para games and Sunway Hotel Georgetown on stronger leisure segment, (iii) office segment with positive growth from all assets save for Wisma Sunway on a slight tenant downsizing, but occupancy is expected to improve gradually to 99% by 4Q18, and (iv) other segments (+20.8%) from the completion of the acquisition of the Shah Alam Industrial asset in August 2017.

Net profit interest (NPI) margins improved by four percentage points (ppts) on lower maintenance expenses at Sunway Pyramid. All in, RNI was up by 18% on slightly lower expenditure (-17%) and despite higher financing cost (+11%) from Shah Alam Industrial asset. Quarter-on-quarter, GRI was up (+7%) driven mostly by: (i) retail segment (+2.7%), and (ii) hotel segment (+27.7%) on similar reasons mentioned above, (iii) other segments on inclusion of the Shah Alam Industrial asset, while (iv) the office segment was flattish.

NPI margins also improved +4.3ppts due to similar reasons mentioned above, allowing RNI to increase by 18%.

FY18E capital expenditure will mostly be for Sunway Carnival Extension in second half 2018 (2H18). As such, we are expecting RM60-RM100 million in FY18-FY19E. FY18-FY19E has minimal leases up for expiry at 17.5%-12% of NLA (net lettable area). We expect mid-to-single digit reversions for retail and low- to-mid single-digit reversions for office assets, while we expect flattish growth for the hospitality segment’s average room rates. Maintain FY18-19E of RM294-298 million, which translates into FY18-19E net dividend per unit of 9.0-9.1 sen (5.2-5.3% net yield).

Our applied spread is close to retail mortgage real estate investment trust (MREIT) peers’ average yield of 5.4% due to the large portion of earnings driven by its stable retail component, while we have already priced in earnings fluctuations in the office and hotel segments.

At current level, Sunway REIT is commanding gross yields of 5.8% (on FY18E), which is slightly better than MREIT peers (>RM1 billion market cap) at 5.7% and retail MREITs of 5.4%, warranting an “outperform” call. Risks to our call include: (i) bond yield expansion, (ii) earnings risks in hospitality and office division, and (iii) lower-than-expected contribution from Sunway Putra Place. — Kenanga Research, Nov 1

This article first appeared in The Edge Financial Daily, on Nov 2, 2017.

For more stories, download EdgeProp.my pullout here for free.

TOP PICKS BY EDGEPROP

Menara HLX (formerly Menara HLA)

KL City Centre, Kuala Lumpur

Monterez Golf & Country Club

Shah Alam, Selangor

Merdeka 118 @ Warisan Merdeka 118

Kuala Lumpur, Kuala Lumpur

Bangunan Setia 1

Damansara Heights, Kuala Lumpur

{kind=link}