Gabungan AQRS Bhd (March 14, RM1.28)

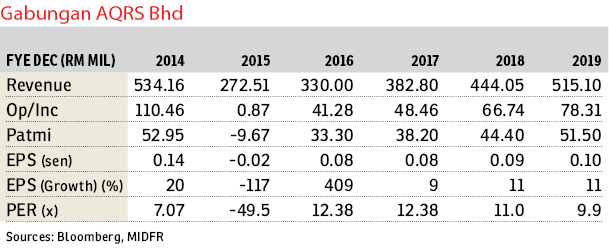

Downgrade to neutral with a target price (TP) of RM1.24: We are prompted to reassess our view on Gabungan AQRS Bhd as its share price has recently traded in line with our TP. Recall that AQRS’ current order book is RM1.8 billion, and it posted a commendable earnings of RM22.7 million (+336% year-on-year) for financial year 2016 (FY2016). Additionally, we reasoned in our previous report on Feb 24 that management had shown their mettle in turning around the company. Hence, we are not surprised that its share price has surged +37.02% year-to-date.

However, AQRS’ earnings estimate remains intact. Despite the rising share price, we are adamant in maintaining our earnings forecasts for AQRS for FY2017/FY2018. At the time of writing, AQRS’ price-earnings ratio (PER) was 21.79 times, which we reckon has run up sharply above our conservative estimate for small- and mid-cap construction companies of 12 times PER. We will shift our view in two scenarios: the order book replenishment rate exceeding the target of RM600 million by +20% or RM720 million for FY2017 and an adjustment to our discounted cash flow (DCF) valuation by increasing our risk-adjusted cash flow forecast from 40% to 55%. This is to comfort any “hard landings” of revenue recognition gaps between the second quarter of FY2017 (2QFY2017) and 4QFY2017, resulting in earnings blips.

We are also mindful of packages under the recently announced alignment of East Coast Railway Link, where one of the Kuantan stations is located in Kota Sultan Ahmad Shah (Kota SAS). Note that AQRS chief executive officer Datuk Azizan Jaafar owns a direct stake of 10.8% in Tanah Makmur KotaSAS Sdn Bhd. Consequently, AQRS potentially stands to benefit from future development in Kota SAS, especially transit-oriented development projects. Additionally, packages of the precast segment for Pan Borneo Highway in Sabah are expected to lend further support to AQRS in FY2018. We are estimating RM400 million worth of orders within the construction period.

We downgrade our recommendation to “neutral” with a TP of RM1.24 based on DCF valuation. — MIDF Research, March 14

This article first appeared in The Edge Financial Daily, on March 15, 2017.

For more stories, download TheEdgeProperty.com pullout here for free.

TOP PICKS BY EDGEPROP

Apartment Tanjung Puteri Resort

Pasir Gudang, Johor

Rawang Integrated Industrial Parks

Rawang, Selangor

Kampung Baru Sungai Buloh

Sungai Buloh, Selangor

Bandar Baru Sri Petaling

Bandar Baru Sri Petaling, Kuala Lumpur

Jalan Klang Lama

Jalan Klang Lama (Old Klang Road), Kuala Lumpur

{kind=link}