Protasco Bhd (Jan 4, RM1.19)

Trading buy call with a fair value of RM1.52: We believe Protasco Bhd is an undervalued gem, especially for its niche business specialising in roadwork maintenance, which provides a steady income stream, as most of its maintenance works are based on concessions awarded by state and federal governments.

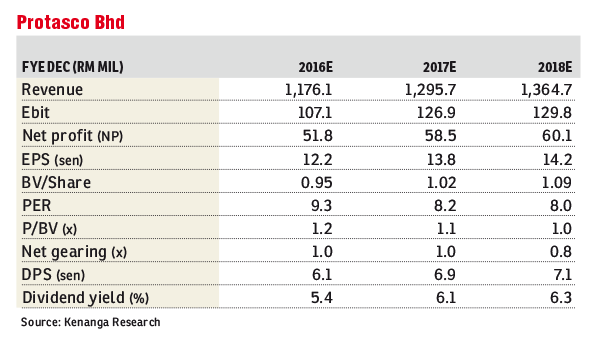

We are projecting steady earnings growth of 13%-3% for financial years 2017-2018 (FY2017-FY2018) backed by both its existing and maintenance order books. We also like it for its decent dividend yield of 6.1% for FY2017.

Protasco is a well-established player in the construction industry where its forte is in road maintenance works on top of several business divisions. Its road maintenance division made up 52% and 69% of its FY2015 revenue and profit before tax respectively, while pre-tax margins are superior at an average of 10% to 13% compared with the conventional construction pre-tax margin that averages around 6%.

As of the cumulative nine months of 2016 (9M2016), Protasco has an outstanding maintenance order book of RM4.4 billion that would last until 2026, contributing RM400 million per annum to its top line.

The maintenance order book comprises concessions awarded by both states and federal governments to carry out routine and periodic road maintenance works over the awarded concession period.

Looking forward, management indicate that their core focus is still road maintenance works, and they are eyeing more sizeable concessions, which could potentially contribute another RM100 million to RM200 million per annum to its top line.

That aside, they are currently bidding for RM300 million worth of state, rural and municipal road maintenance contracts. For its construction division, management is targeting a replenishment of RM500 million for FY2017 that comprises infrastructure and government housing projects such as PPA1M (1Malaysia Housing Projects for Civil Servants).

We believe that management’s target is not overly ambitious and is highly achievable given its tender book size of RM5 billion. Furthermore, Protasco has a strong track record with the PPA1M programme, in which they have thus far bagged two phases of PPA1M with a cumulative value of RM900 million.

Over the past five years, Protasco has been consistently paying out more than 60% of its net profit as dividends, albeit not having a formal dividend policy. We note that it is at the higher end in terms of payout among contractors.

At our conservative dividend payout ratio assumption of 50%, we would be expecting dividend per share of 6.9 sen for FY2017, which translates into a yield of 6.1%, which is far superior compared with its small- to mid-cap peers’ average of 2.9%.

While net gearing may seem high at 1.2 times as of 9MFY2016, this is due to the project financing for Phase 1 of PPA1M of which management is expecting a bullet repayment of about RM525m from the government upon completion.

The group’s 9MFY2016 net profit declined by 10% as its pre-tax margin was compressed by three percentage points to 9% due to non-renewal of two state road maintenance contracts during the year.

We are projecting a net profit growth of 13%-3% for FY2017-FY2018E (estimate), which is backed by i) its outstanding order book of RM742 million with replenishment assumptions of RM500 million per annum for FY2017-FY2018E, ii) an outstanding maintenance order book of RM4.4 billion that would last it for another 10 years, and iii) property unbilled sales and inventories worth RM113 million, while growth assumptions for other divisions are flattish.

We value Protasco at RM1.52 based on 11 times FY2017E price- earnings ratio that is within our mid-cap peers’ range of 11 times to 13 times.

We see room for upgrade in valuations should Protasco be able to pare down its debts upon receiving the bullet repayment for its PPA1M project by the end of the first half of 2017, which would bring its net gearing into net cash.

Furthermore, the potential rerating catalyst for Protasco would be firstly higher-than-expected replenishments of more than RM500 million, potential extra emergency road maintenance works to be carried out should the 14th general election be called in 2017. Currently, its dividend yield of 6.1% is still far superior compared with its mid-cap peers’ average of 2.9%. — Kenanga Research, Jan 4

This article first appeared in The Edge Financial Daily, on Jan 5, 2017. Subscribe to The Edge Financial Daily here.

TOP PICKS BY EDGEPROP

Bandar Baru Wangsa Maju (Seksyen 6)

Wangsa Maju, Kuala Lumpur

Pangsapuri Mawar Sari

Taman Setiawangsa, Kuala Lumpur

{kind=link}