Banking sector

Maintain overweight: June 2016 loan growth (+5.6% year-on-year) saw yet another subdued month as business loan growth and household loan growth continue to trend lower. The annualised system loan growth remained weak at 2.8% mainly due to the weak growth in the first four months of the year.

However, we note that June’s loan growth continued the positive momentum seen in May, as business loan growth year to date turned positive for the first time in 2016 while loan applications, approvals and disbursement levels also showed some encouraging signs.

We retain our loan growth forecast of 6% for 2016 (based on 6.4% growth from the household sector and 5.5% from business sector) as we believe that the general strength in the domestic economy, with a low unemployment rate of 3.4% (May 2016), coupled with sufficient liquidity in the banking system and a more accommodative monetary policy should continue to support credit growth in 2016.

We also do not rule out a more aggressive upcoming fiscal budget 2017 ahead of a possible national election next year although any positive spillover effects are likely to be more apparent towards the end of 2016 and 2017. With the recent cut in the overnight policy rate (OPR), most banks have reduced their base rate by 15 basis points (bps) to 25 bps. We believe that this is positive for business loan growth, especially with the expected commencement of some major infrastructure projects in second half of 2016 (2H16).

Meanwhile, effects on household loans are likely to be more subdued as banks remain cautious about the approval of residential loans amid a high household debt to gross domestic product level.

National Property Information Centre primary property market preliminary data also showed that overall units launched and sold in 1H16 plunged to 10,655 units (1H15: 49,280 units) and 2,732 units (1H15: 23,909 units) respectively (Source: TheEdgeProperty.com).

Therefore, the 25 bps OPR cut may not be significant enough to boost the fragile confidence among property developers and buyers. Nevertheless, the OPR cut in general still represents positive news for the ailing property market.

The industry loan loss cover slid to 89.5% as system gross impaired loan ratio continued to see a slight uptick to 1.66%, as at June 2016. Key sectors which remain vulnerable include construction, manufacturing and transport, storage and communication. On a more positive note, feedbacks from management of local banks have indicated that a lower loan loss cover is a result of better collaterised impaired loans. With less provisions set aside, we do not foresee any significant negative surprise in terms of credit cost for the upcoming 2Q16 results for the sector.

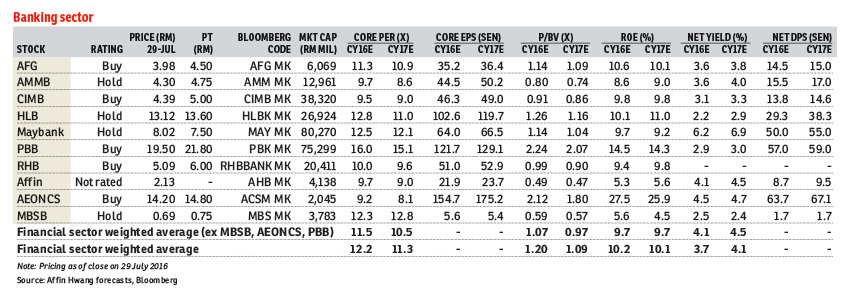

We note that overall sector valuation for banks in 2016 remains quite attractive at a 1.07 times price to book value (P/BV) multiple versus the 3-year average of 1.5 times. For sector exposure, we expect CIMB Group Holdings Bhd (“Buy”, RM4.39; target price [TP] of RM5 at 1 time P/BV) to see a more significant turnaround in 2016 estimated earnings in the absence of staff rationalisation cost and hefty provisions at PT CIMB Niaga Tbk.

For RHB Bank Bhd (“Buy”, RM5.09; TP of RM6 at 1.15 times P/BV), we expect an improved earnings profile with a relatively steady net interest margin as well as better asset quality and strengthened capital ratios post-rights issue and internal restructuring.

Moreover, we continue to like defensive banks such as Public Bank Bhd (“Buy”, RM19.50; TP of RM21.80 at 2.5 times P/BV) given the group’s more stringent credit underwriting standards and established franchise in the domestic retail financing markets. We also like Alliance Financial Group Bhd (“Buy”, RM3.98; TP of RM4.50 at 1.36 times P/BV) as a niche and nimble small-cap bank — AffinHwang Capital, Aug 1

This article first appeared in The Edge Financial Daily, on Aug 2, 2016. Subscribe to The Edge Financial Daily here.

TOP PICKS BY EDGEPROP

The Hipster @ Taman Desa

Taman Desa, Kuala Lumpur

Subang Jaya City Centre (SJCC) : Teja

Subang Jaya, Selangor

Seksyen 51, Petaling Jaya

Petaling Jaya, Selangor

Villa Heights @ Equine Park

Seri Kembangan, Selangor

Aliran Damai, Bandar Damai Perdana

Cheras South, Kuala Lumpur

Aliran Damai, Bandar Damai Perdana

Cheras South, Kuala Lumpur

Tembikai Court, Taman Universiti Indah

Seri Kembangan, Selangor

Aliran Damai, Bandar Damai Perdana

Cheras South, Kuala Lumpur

Long Branch Residences

Kota Kemuning, Selangor

{kind=link}