Eco World Development Group Bhd, June 29 (RM1.26)

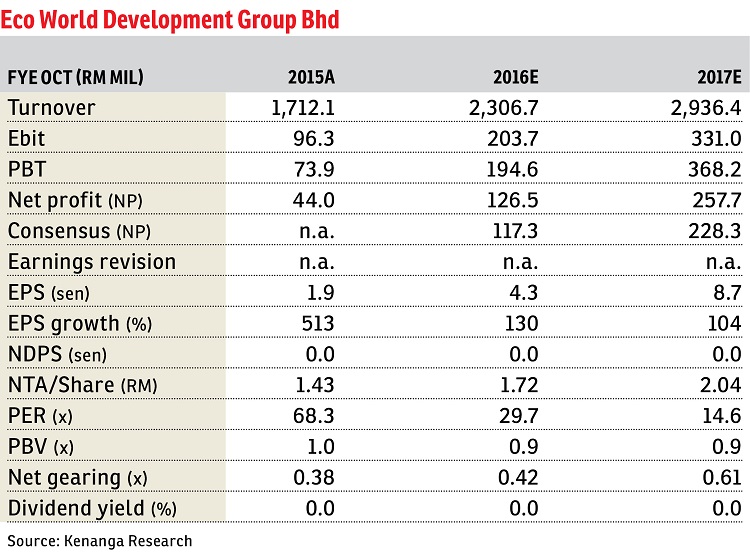

Maintain outperform with a higher target price (TP) of RM1.58: Eco World Development Group Bhd’s (EcoWorld) first half of 2016 (1HFY16) earnings of RM55.3 million made up 47% and 44% of the street’s and our expectations respectively. We expect a stronger billing cycle in 2HFY16 as project handovers take place. Seven months of 2016 (7M16) sales of RM1.32 billion made up 33% of management’s and our FY16 estimated sales target of RM4 billion. We deem this broadly in line in terms of local sales as the target includes about 25% of sales from its soon-to-be listed associate, Eco World International Bhd (EWI), which has raked up RM1.45 billion sales for 5M16. Management maintains its estimated FY16 to FY17 sales target at RM4 billion to RM4.5 billion. No dividends were declared.

Its 1HFY16 bottom line leaped by 272% year-on-year, largely due to the normalisation of billings from new sales garnered when EcoWorld was established. Second quarter of 2016 earnings were up by 68% quarter-on-quarter (q-o-q) to RM34.7 million on improved billings (+33%) and earnings before interest and tax margins (+2 percentage points q-o-q to 9.8%) on controlled sales/marketing and administrative expenses, which were consistent with management’s earlier guidance.

The group announced the acquisition of 374.6 acres (151.6ha) of land in Batu Kawan for RM875.2 million, with a gross development value (GDV) of RM7.8 billion. It also updated on its Kuala Selangor land (2,198.4 acres at RM1.18 billion; GDV of RM15.3 billion) and approvals appear to be in place. EcoWorld will be using its “Partnership for Growth Model” where it invites strategic investors to participate, and we gather that the Employees Provident Fund has expressed interest. Its 25% placement should be completed soon.

The listing of EWI has been slightly delayed to September or October 2016 due to a “new strategic investor”, while management is unfazed by Brexit. Factoring in all these exercises, we expect its FY17 net gearing to increase from 0.44 times to 0.61 times. Overall, we view this exercise and business model as a positive as it allows the group to expand its presence and branding quickly, and also globally without overtaxing its balance sheet, while leveraging the different strengths and expertise of its strategic partners. Note that landbanking activities are expected to continue (it was reported that EcoWorld may revisit the Eco Marina deal), but management indicated that it is exploring non-dilutive fund raising options.

There’s no changes in our earnings estimates, while its unbilled sales of RM4.5 billion provide about 1.5 years of visibility.

We maintain “outperform” with a higher TP of RM1.58 (from RM1.49). Our FD sum-of-parts (SOP) has been increased by 7% to RM2.92 as i) Eco World’s stakes in Eco Horizon/Sun and Eco Gardens/EBPV are at 60% each; and ii) our earlier estimates included Eco Ardence at a 50% stake, and EWI at a 30% stake with a 25% placement to raise approximately RM768 million. Our TP is increased to RM1.58, based on an unchanged 51% property revalued net asset valuation discount (implied FD SOP discount is 45%).

The group is set to benefit from a few major news flows this year, particularly since there is no major excitement in the sector. — Kenanga Research, June 29

This article first appeared in The Edge Financial Daily, on June 30, 2016. Subscribe to The Edge Financial Daily here.

TOP PICKS BY EDGEPROP

Aster Grove Residences Park

Shah Alam, Selangor

Bandar Baru Wangsa Maju (Seksyen 2)

Wangsa Maju, Kuala Lumpur

{kind=link}