Sunway Real Estate Investment Trust (April 26, RM1.87)

Maintain buy with a higher target price (TP) of RM2.02: Sunway Real Estate Investment Trust (REIT) has completed the acquisition of its first education asset for RM550 million. Of the full amount, RM340 million is funded through perpetual note programme (perps). We think that the coupon rate for the perps will be higher than its existing loan interest rates of slightly over 4% but the purchase should still be earnings-accretive as the debt-to-equity ratio is 38:62.

We estimate that the new asset will make up about 5% of Sunway REIT’s total revenue for financial year 2020 forecast (FY20F). Earnings contribution for FY19F is expected to be limited to two months. We also expect one-off fees arising from the establishment of the perps to be minimal and will most likely be offset by the positive contribution of the asset.

We expect the upcoming quarter core net income to be on par with the set of numbers in the previously corresponding period. We expect this to be supported by positive rental income growth from Sunway Pyramid.

Meanwhile, the improved office segment is offset by the weaker performance from the hotel segment. That said, the refurbishment work at Sunway Resort and Spa had come to an end towards end-2018 and we expect recovery in revenue from the hotel going forward earnings for FY20F up by 1% to factor in the inclusion of the education asset.

Looking ahead, we expect Sunway REIT to continue to balance its portfolio in order to achieve earnings accretion in the long run. This may include further acquisition of more assets from the “others” segment.

Currently, Sunway REIT owns The Sunway Medical Centre, an industrial asset in Shah Alam and the education property other than its retail, hotel and office segments. We are positive about this strategy as the long-term tenancy agreement from this category may buffer the income volatility of the hotel segment, thus providing better stability for the REIT. Subsequently, we have included the contribution from the education asset into our earnings estimate for FY20F but leave FY19F estimate unchanged.

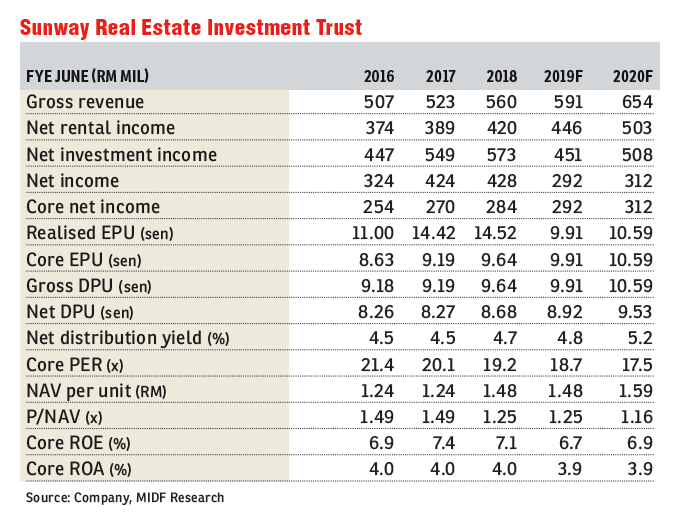

Maintain “buy” with adjusted TP of RM2.02 as we roll over our base year. Our dividend discount model-based valuation (required rate of return of 7.4%; terminal growth rate of 2%) is maintained. We like Sunway REIT for its integrated asset cluster in a mature township and stable prospects from its crown jewel Sunway Pyramid Mall. Dividend yield is estimated at 4.8%. — MIDF Research, April 26

This article first appeared in The Edge Financial Daily, on April 29, 2019.

Click here for more property stories.

TOP PICKS BY EDGEPROP

Apartment Tanjung Puteri Resort

Pasir Gudang, Johor

D'Ambience Residences (Ikatan Flora), Bandar Baru Permas Jaya

Permas Jaya/Senibong, Johor

{kind=link}