UEM Edgenta Bhd (Oct 5, RM2.70)

Initiate coverage with buy and a target price (TP) of RM3.22: UEM Edgenta Bhd is Malaysia’s largest integrated facilities management (IFM) provider. Its expertise covers consultancy, services and solutions for the healthcare, infrastructure and real estate segments. We expect the group to continue benefiting from Malaysia’s growing IFM market, which had previously recorded a decent 7.9% compound annual growth rate (CAGR) over the last five years. Frost & Sullivan estimated for this market to earn increased revenue of up to RM7.43 billion in 2022 (2017: RM4.79 billion) — a robust CAGR of 9.2% for this period.

UEM Edgenta’s infrastructure wing is set to embark on a performance-based contracting (PBC) framework for the network management and maintenance of the North-South Expressway (PLUS). Phase 1 is set to commence in the second half of 2018 and will be fully implemented by 2019. Under this new PBC approach, fees are linked to performance — the infrastructure business is to transform its expressway maintenance delivery model into an outcome/performance-based one from an input/resource-based variant.

There is potential for Edgenta’s subsidiary Edgenta Propel Bhd to win the maintenance work contract for the Pan Borneo Highway Sabah project, despite the possibility of a change in the project delivery partner model.

This is because another subsidiary — Opus International (M) Bhd — is a consultant for this development, giving UEM Edgenta an advantage in terms of winning the maintenance work concession for this project.

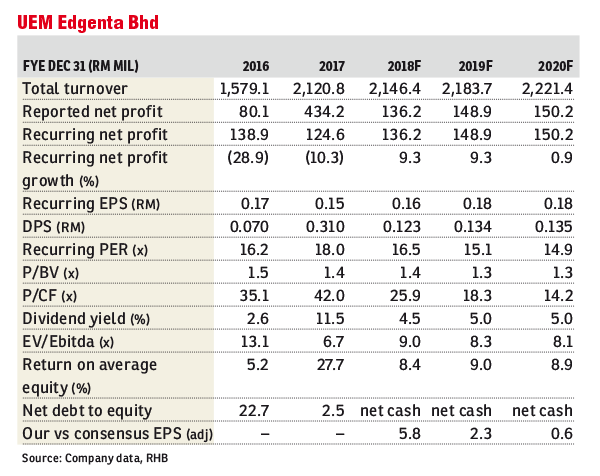

The group has a policy of paying out between 50% and 80% of its profit after tax and non-controlling interest as dividends. We estimate for financial year 2018 (FY18) to FY19 dividends per share of 12.3 sen and 13.4 sen, which translate into decent yields of 4.5% and 5% respectively. We believe this generous dividend payout will continue in view of the group’s healthy cash flow and sturdy balance sheet.

We initiate coverage with “buy” and a TP of RM3.22, with a 19% upside. Our discounted cash flow-derived TP implies an FY19 forecast price-earnings ratio (PER) of 18 times, close to +1 standard deviation of its historical one-year forward PER average of 19 times. We believe this is fair, given the expected five-year earnings before interest, taxes, depreciation, and amortisation CAGR of 12% and when compared to peers’ one-year forward PER of 17.5 times. Note that this stock is under-researched: We are one of only three brokers covering it.

Risks to our call include the abolishment of toll concessions, a cancellation or delay of the Pan Borneo Highway initiative, and further increases in the national minimum wage, which should raise subcontractor costs. — RHB Research Institute, Oct 5

This article first appeared in The Edge Financial Daily, on Oct 8, 2018.

TOP PICKS BY EDGEPROP

Taman Perindustrian Desa Cemerlang

Ulu Tiram, Johor

Seri Mutiara Apartment, Bandar Baru Seri Alam

Masai, Johor

De Bayu Apartment @ Setia Alam

Shah Alam, Selangor

3 Storeys Bungalow Taman OUG KL

Taman OUG, Kuala Lumpur

{kind=link}