Kimlun Corp Bhd (June 21, RM1.39)

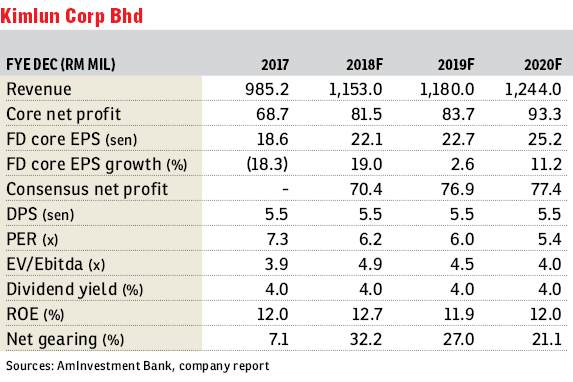

Maintain buy with a fair value (FV) of RM1.81: Our FV is based on eight times financial year 2019 forecast (FY19F) earnings per share (EPS). Kimlun has secured a RM53.5 million contract for infrastructure works for the Gerbang Nusajaya Development in Johor. This is the second key construction job Kimlun has secured in FY18, boosting its year-to-date construction job wins to RM197.6 million and its construction order book to RM2 billion. We are keeping our forecasts that assume construction job wins of RM700 million annually in FY18F to FY20F.

Prospects for the local construction sector are unfavourable, as the government is reconsidering various mega infrastructure projects. Besides the Kuala Lumpur-Singapore high-speed rail and mass rapid transit 3, we believe more megaprojects could be deferred, scaled down or cancelled.

But we believe the selldown in Kimlun shares has been overdone. It is trading at six times its FY19F fully diluted EPS, below our benchmark forward target price-earnings ratio of seven to nine times for small-cap construction stocks.

Kimlun’s construction and manufacturing order backlogs are at RM2 billion and RM421 million respectively, which will keep it busy for the next one to two years. Despite the local public job cutbacks, we believe Kimlun’s earnings could be sustained as it depends largely on private-sector building jobs, and orders for its precast concrete segment from infrastructure projects in Singapore. — , June 21

This article first appeared in The Edge Financial Daily, on June 22, 2018.

For more stories, download EdgeProp.my pullout here for free.

TOP PICKS BY EDGEPROP

Sunsuria Forum @ 7th Avenue

Setia Alam/Alam Nusantara, Selangor

Setia Damai

Setia Alam/Alam Nusantara, Selangor

Taman Bukit Senawang Perdana

Seremban, Negeri Sembilan

Taman Sijangkang Jaya

Telok Panglima Garang, Selangor

Saffron Hills @ Denai Alam

Denai Alam, Selangor

Primaya Bandar Tun Hussein Onn

Cheras, Selangor

Jalan Setiawangsa

Taman Setiawangsa, Kuala Lumpur

{kind=link}