Kerjaya Prospek Group Bhd (Jan 4, RM4.11)

Maintain underperform with an unchanged cum/ex target price (TP) of RM3.40/RM1.55: Yesterday, Kerjaya Prospek Group Bhd proposed for a bonus issue of 677.4 million bonus shares on the basis of six bonus shares for every five existing shares and 169.4 million free warrants on the basis of six free warrants for every 20 existing shares.

The tentative exercise price for the free warrants is at RM1.59 with a tenure of five years. The corporate exercises are expected to be completed by the first quarter of 2018 (1Q18).

We were not surprised by the proposed exercises as we have been anticipating it since mid-financial year ending Dec 31, 2017 (FY17).

We remain neutral on the exercises as there’s no fundamental change towards the earnings outlook for Kerjaya. That said, the proposed bonus issuance will improve the share liquidity that in turn provides for greater participation by the investment community.

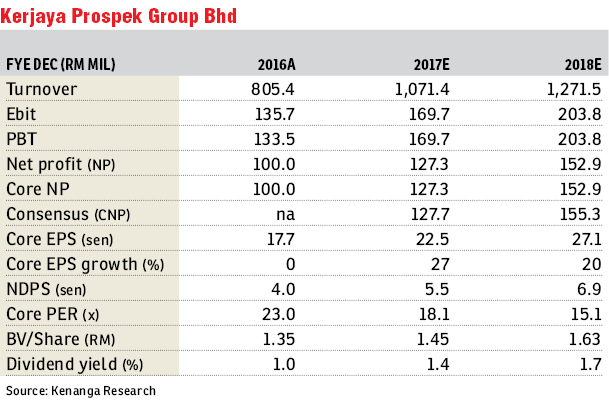

For FY18, we are anticipating Kerjaya to clinch new wins of RM1.2 billion. They have secured RM1.4 billion contract wins in FY17, meeting our expectations of RM1.4 billion.

Currently, Kerjaya’s outstanding order book stands at RM3.2 billion, giving them a visibility of about 2.5 to three years.

Meanwhile, its tender book stands at about RM1 billion. We believe further project wins could likely stem from its major shareholder Datuk Tee Eng Ho’s private property arm, which is planning to launch a mixed development project at Old Klang Road with a gross development value (GDV) of RM1 billion. This may lead to about RM300 million to RM400 million worth of construction contracts likely to be dished out in FY18.

We maintain our FY17 to FY18 earnings of RM127 million to RM153 million post announcement based on the FY17/FY18 replenishment target of RM1.4 billion/RM1.2 billion.

We maintain “underperform” with an unchanged cum/ex TP of RM RM3.40/RM1.55 as we believe that Kerjaya’s risk-to-reward ratio is no longer compelling as it is currently trading at a FY18 price-earnings ratio (PER) of 15.1 times, implying a FY18 construction PER of 16 times — which we consider high as it is above our ascribed range of eight to 13 times for small mid-cap contractors within our universe.

We believe further rerating catalysts for Kerjaya could be higher-than-expected replenishment or profit margins. — Kenanga Research, Jan 4

This article first appeared in The Edge Financial Daily, on Jan 5, 2018.

For more stories, download EdgeProp.my pullout here for free.

TOP PICKS BY EDGEPROP

Foresthill Residences

Damansara Perdana, Selangor

Bandar Puteri Puchong, Hill Top 2sty Freehold Terrace Landed House 4R4B NonBumi, bandar puchong jaya, taman wawasan, bandar kinrara, puchong hartamas,

Bandar Puteri Puchong, Selangor

Jalan Chow Kit / Jalan Putra

KL City, Kuala Lumpur

Rawang Integrated Industrial Parks

Rawang, Selangor

Jalan Klang Lama

Jalan Klang Lama (Old Klang Road), Kuala Lumpur

{kind=link}