Mah Sing Group Bhd (Oct 20, RM1.58)

Downgrade to market perform with an unchanged target price of RM1.63: Mah Sing Group Bhd has terminated the Titiwangsa land deal worth RM60 million as the resolution of competing ownership claims will be long drawn.

While this surprised us, it was an understandable move as Mah Sing prefers to concentrate its capital on immediately developable projects. There is no major impact on its revalued net asset value, net gearing or earnings. We expect more landbanking activities in the Klang Valley soon.

Mah Sing announced that it had terminated the sale and purchase agreement to acquire 3.56 acres (1.44ha) of freehold residential land (RM60 million land cost, RM650 million gross development value [GDV]) in Titiwangsa, Kuala Lumpur, due to non-fulfilment of conditions precedent during the said period. The vendor of the land shall refund the deposit of RM6 million to Mah Sing.

Recall that shortly after the acquisition was announced, the Titiwangsa land was faced with competing claims on the rightful ownership of the land, and we gather that ascertaining ownership will be a very long-drawn process.

We were surprised by the news as Mah Sing had indicated that it was very keen on this prime piece of land and was willing to buy it from the rightful owner. However, if the competing claims on the land drag on for too long, it will tie up balance-sheet commitment of the group, which could be deployed for projects that are immediately developable. Since the authorities were unable to provide a timeline on when this ownership issue can be settled, Mah Sing believes it is best to move on.

We expect more Klang Valley mass market-driven projects to be secured over the next six to 12 months, and have built in a GDV replenishment assumption of RM2.2 billion. We also believe that second half of financial year 2017 (2HFY17) launches will exceed that of 1HFY17.

Besides continuous efforts to clear inventories and work in progress, key new launches in 2HFY17 include M Vertica @ Cheras, M Centura @ Sentul, iParc @ BukitMertajam, Penang, M Aruna @ Rawang, while it also pushes out new phases of ongoing projects like Southville (Savanna 2), Southbay (M Vista) and Meridin East (Phase 2 of Fern).

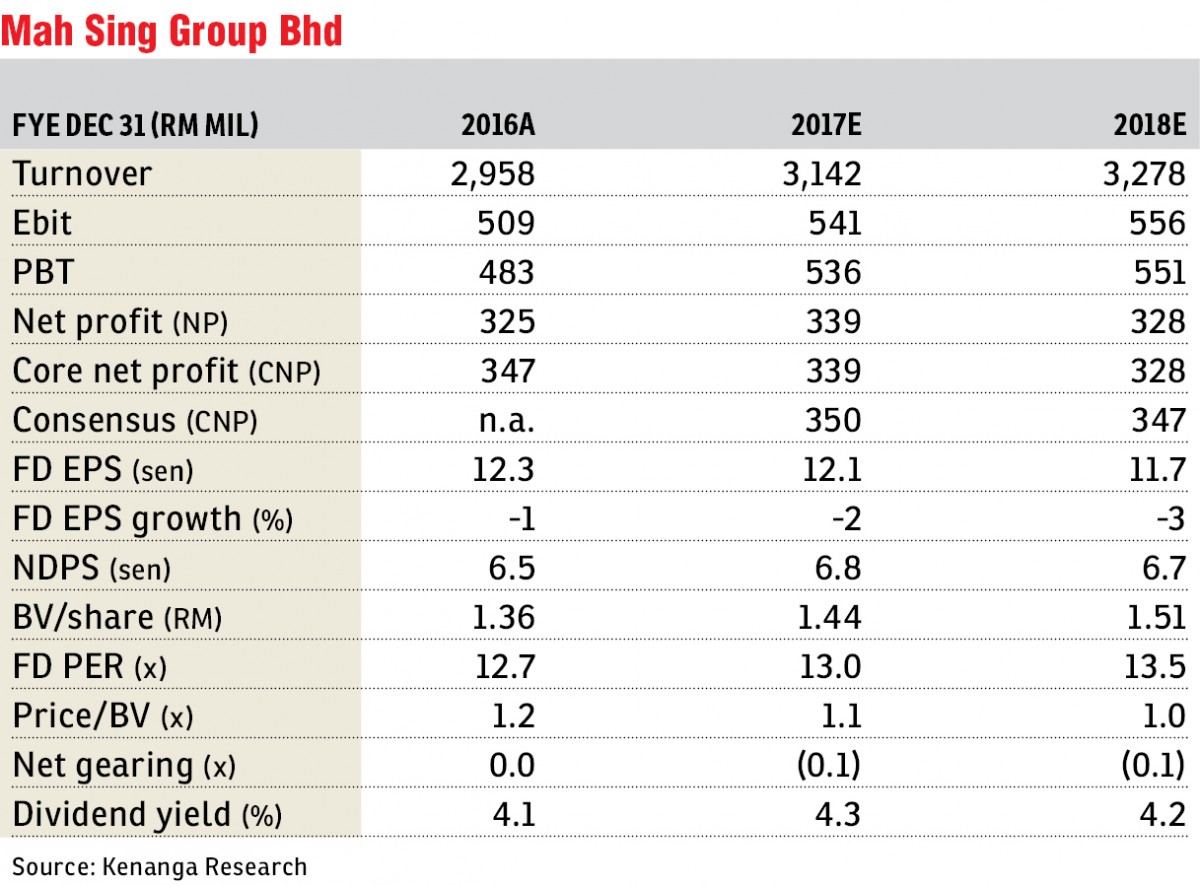

There is no change to our earnings forecasts, as significant contribution from the Titiwangsa land was only timed for FY19 onwards. Unbilled sales of RM3.02 billion provide more than one year’s visibility. While we remain optimistic about potential land deals, we note that its share price has recently done well and thus, we downgrade our call to “market perform” from “outperform”.

We may review our call with an upside bias once the group is able to secure new land bank and launch it within 12 months of acquisition, or if its share price has corrected sharply. Its yield of 4.3% is above big-cap developers’ (over RM3 billion market capitalisation) average yield of 3% and should offer downside support.

Risks include: i) weaker-than-expected property sales, ii) margin issues, iii) negative real estate policies; and iv) deterioration in the lending environment. — Kenanga Research, Oct 20

This article first appeared in The Edge Financial Daily, on Oct 23, 2017.

For more stories, download EdgeProp.my pullout here for free.

TOP PICKS BY EDGEPROP

Taman Impian Indah, Cheras

Cheras South, Selangor

Pearl Suria

Jalan Klang Lama (Old Klang Road), Kuala Lumpur

SU1 @ Bandar Saujana Utama

Sungai Buloh, Selangor

Encorp Strand Garden Office

Petaling Jaya, Selangor

VIVO Residential Suites

Jalan Klang Lama (Old Klang Road), Kuala Lumpur

The Grand @ Kelana Damansara Suite

Kelana Jaya, Selangor

Bandar Botanic

Bandar Botanic/Bandar Bukit Tinggi, Selangor

{kind=link}