Pavilion Real Estate Investment Trust (July 28, RM1.75)

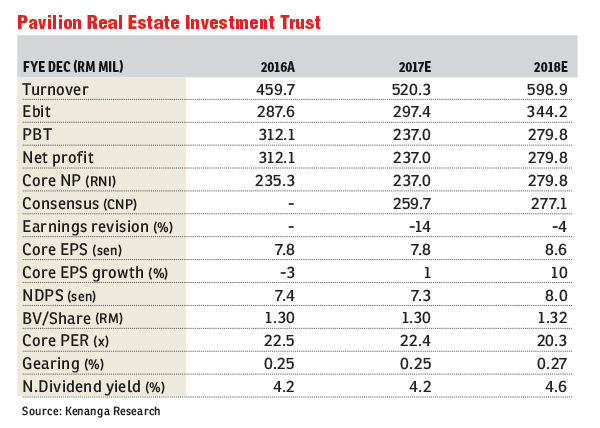

Maintain outperform with a lower target price (TP) of RM1.85: Pavilion Real Estate Investment Trust’s (REIT) realised net income (RNI) for the first half financial year 2017 (1HFY17) of RM111.4 million came in below both consensus and our expectations at 43% and 40%, respectively. The 1HFY17 gross dividend per unit (GDPU) of 3.96 sen per unit (which included a non-taxable portion of 0.13 sen) was also below expectations at 42% of our FY17 GDPU of 9.4 sen (4.9% dividend yield). Although the top line came in within our expectations at 46%, results missed due to margin compressions from higher operating and financing costs.

Year-on-year, gross rental income was up by 6% on the acquisition of Damen Mall and Intermark Mall (in March 2016), and positive rental growth from other assets on mid-single-digit reversions. However, RNI declined by 8% on higher operating cost (+23%) on maintenance cost for the air-conditioning system and upgrading work, air chillers’ rewinding, replacement of escalator handrails and broken combs at Pavilion Mall, replacement of lift and escalator parts and improvement of light fittings at Intermark Mall, and tenancy costs incurred for landlord provisions at Damen Mall, and higher expenditure (+4%), and higher financing cost (+30%) incurred for the acquisitions of the new malls. On a quarter-on-quarter basis, RNI for the second quarter of FY17 (2QFY17) declined by 5% on the back of a marginal top-line growth (1%) from positive reversions, but the bottom line succumbed to margin pressure due to a higher operating cost (+9%) on the aforementioned reasons.

Pavilion REIT has also announced the proposed acquisition of Elite Pavilion with Urusharta Cemerlang (KL) Sdn Bhd (UCKL) and a vesting agreement with Urusharta Cemerlang Sdn Bhd (UCSB) and UCKL for extension connections for the RM580 million purchase considerations. Additionally, Pavilion REIT has also announced a conditional sale and purchase agreement with UCSB for the disposal of 10 car park bays for RM880,000. We believe the asset net property income (NPI) yield is decent at 6.1% considering tough market conditions versus Pavilion REIT’s intended target of 6.5%, while Pavilion Kuala Lumpur mall’s NPI yield is 6.0% (at FY16). The acquisition is expected to be completed in 4QFY17 and will be funded by a combination of borrowings and 7.2% placement. All in, we are positive about this acquisition as it contributes about 8% to FY18 earnings and 7.6% to distribution per unit post placement.

We apply the thinnest yield spread among Malaysian REITs under our coverage as we believe Pavilion REIT should be traded at thinner spreads on strong catalyst from expectations of asset injections. As such, we believe Pavilion REIT warrants an “outperform” call, with an attractive total return of 11% at current level. Risks to our call include bond yield expansion versus our target 10-year Malaysian Government Securities yield, and weakening rental income. — Kenanga Research, July 28

This article first appeared in The Edge Financial Daily, on July 31, 2017.

For more stories, download TheEdgeProperty.com pullout here for free.

TOP PICKS BY EDGEPROP

Subang Perdana Goodyear Court 10

Subang Jaya, Selangor

KL Gateway Premium Residence

Bangsar South, Kuala Lumpur

Impian Bukit Tunku

Kenny Hills (Bukit Tunku), Kuala Lumpur

{kind=link}