Pavilion Real Estate Investment Trust (April 28, RM1.74)

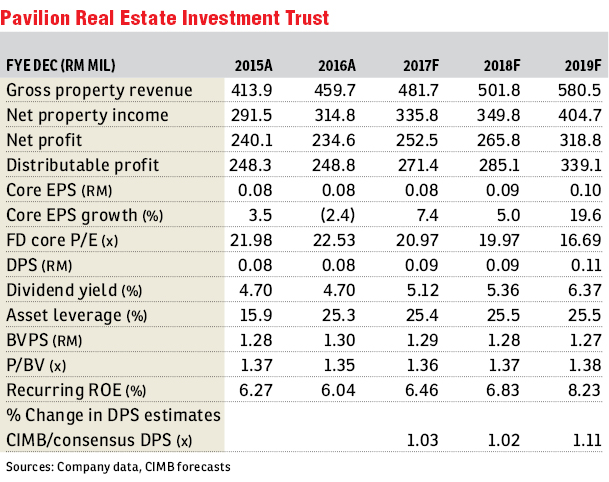

Maintain hold with a lower target price (TP) of RM1.76: While Pavilion Real Estate Investment Trust’s (REIT) first quarter ended March 31, 2017 (1QFY17) revenue rose 11.5% year-on-year (y-o-y) to RM118.9 million, its core net profit dipped 7% y-o-y to RM57 million.

This was broadly in line with our expectations but below Bloomberg and consensus’ expectations, accounting for 23% and 22% of the respective full-year estimates. The 1QFY17 income distribution per unit (DPU) of 2.02 sen for 1QFY17 was broadly in line with our full-year DPU forecast of 8.95 sen.

The group’s 1QFY17 top-line growth of 11.5% y-o-y was attributable to additional income from properties acquired in 1QFY16, namely Da Men Mall, in USJ (Subang Jaya) and Intermark Mall, Kuala Lumpur.

On the other hand, the 7% dip in core earnings was due to a 78% y-o-y surge in borrowing cost to fund the acquisitions.

Pavilion Kuala Lumpur mall (PKL) recorded lower gross revenue (down 2% y-o-y) as the mall is still in the midst of tenant repositioning to improve tenancy mix and we gather this is likely to continue into the first half of 2017.

The 1QFY17 net property income grew 4.4% y-o-y to RM79 million as rental income from the additional assets more than offset the increase in property expenses (up 28.7% y-o-y).

The higher property expenses were on the back of routine operating expenses pertaining to Da Men Mall and Intermark Mall as well as lift and escalator replacements in Intermark Mall.

Management has expended RM1.1 million of its capital expenditure guidance of about RM20 million to continuous toilet upgrading in PKL and adding food and beverage kiosks in Intermark Mall.

We gather that 1QFY17 portfolio rental reversion was a low single digit. In line with management’s guidance, we expect PKL to achieve rental reversion of 2% for the 23% of net leaseable area expiring in FY17 as the majority of expiring leases are for smaller spaces.

While management focuses on improving tenant mix in Da Men Mall to increase footfalls, this could come at the expense of reversions, in our view. Jones Lang Wootton is guiding for flat reversions for suburban malls in the Klang Valley in FY17.

Further details on the potential injection of Pavilion Elite (PE), for which the REIT has rights of first refusal (ROFR), is still scant but management is guiding that this will likely occur by FY17, and an equity-raising exercise remains on the table.

While the group also has ROFR for Fahrenheit 88, the acquisition of this mall is unlikely in the near term, we gather. Management’s main focus for now will be on PE acquisition, which we gather has an occupancy of about 70% currently but could rise to about 85% by year end.

We keep our “hold” call but lower our dividend discount model-based TP to RM1.76 to reflect lower terminal growth assumptions of 1.8% (from 2.5%). We think the stock is fully valued at current levels.

Upside risks to our call include higher rental reversions, especially for PKL, and downside risk is increased competition from suburban malls for Da Men Mall.

We think PKL will be slightly less affected by the incoming retail supply due to its strong tenant profile. — CIMB Research, April 27

This article first appeared in The Edge Financial Daily, on May 2, 2017.

For more stories, download TheEdgeProperty.com pullout here for free.

TOP PICKS BY EDGEPROP

Tujuh Residences @ Kwasa Damansara City Centre

Shah Alam, Selangor

Damansara Seresta

Bandar Sri Damansara, Kuala Lumpur

Alora Residences @ Avenue 25 Subang Jaya

Subang Jaya, Selangor

{kind=link}