Sunway REIT acquires industrial asset for RM91.5 mil

Sunway Real Estate Investment Trust (Jan 12, RM1.72)

Maintain market perform call with a higher target price (TP) of RM1.68: Sunway Real Estate Investment Trust (REIT) has acquired an industrial asset in Shah Alam for RM91.5 million from Champion Edge Sdn Bhd with a long-term lease of 18 years, which we deemed as neutral-to-mildly positive for earnings.

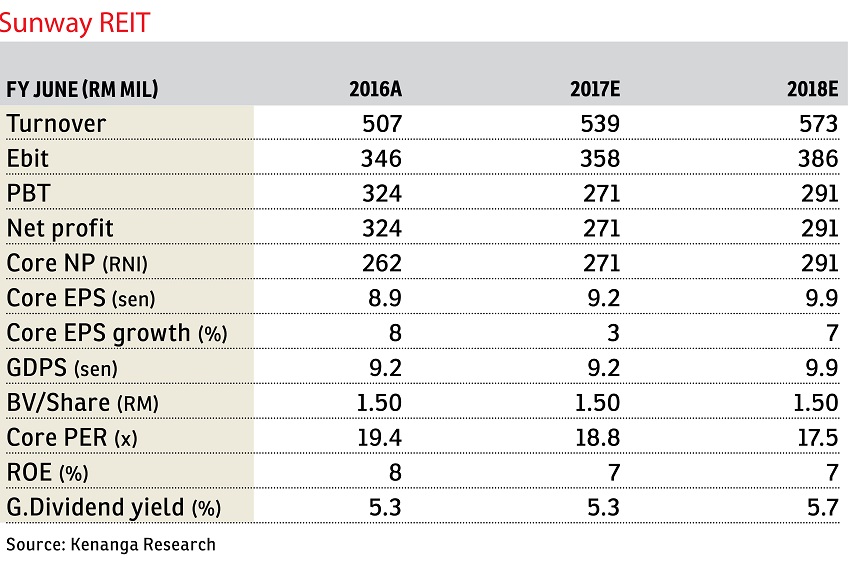

As such, we increase our earnings marginally by less than 1% for financial year 2017 (FY2017) and FY2018. We maintain “market perform” but increase our TP to RM1.68 (from RM1.61), on a slightly lower targeted gross yield of 5.7% (from 5.9%), closer to its Malaysian REIT peers’ average yield of 5.5%.

Sunway REIT has acquired its first industrial asset, which consists of a factory, warehouse and office space with a long-term lease of 18 years until December 2034 (initial term) and a five-year renewal to IDS Manufacturing Sdn Bhd. Rental reversions are every three years (next review in January 2019) with a minimal step up which is capped at a maximum 10%. The acquisition is expected to be completed by the third quarter of FY2017 upon the conditions precedent being met.

The asset’s gross yield and net yield are similar at 6.1% as it is a triple net lease asset, implying that most costs are borne by the tenant. Although this is not as attractive as Axis REIT’s recent industrial asset acquisitions of 7% to 8%, we believe this will help improve Sunway REIT’s portfolio yield of 5.5% in FY2016.

Furthermore, the long lease term of 18 years provides income stability from guaranteed rental to Sunway REIT in tough market conditions due to uncertainty in the office and hospitality segment. Location-wise, the asset is in close proximity to major highways, namely Federal Highway, Elite Highway and Shah Alam Expressway as well as to Kuala Lumpur International Airport and Port Klang.

We are neutral to mildly positive about the acquisition as impact to earnings is minimal at 0.4% to 0.7% in FY2017 to FY2018E (estimated). Post-acquisition, we expect Sunway REIT gearing to inch up slightly to 0.35 times (from 0.34 times currently) as the acquisition is relatively small. This is below Securities Commission Malaysia’s limit of 0.5 times and Sunway REIT’s internal gearing limit of 0.4 times. All in, we are mildly positive about this acquisition despite it being yield-neutral to shareholders as it provides earnings stability in the long run.

As such, we increase our FY2017 to FY2018E average gross dividend per share slightly to 9.6 sen (from 9.5 sen), implying gross yields of 5.3% to 5.7% in FY2017 to FY2018E.

We maintain “market perform” on a higher TP of RM1.68 (from RM1.61) based on a lower FY2017 to FY2018E target gross yield of 5.7% (net: 5.2%). This is based on a lower spread of +1.5 percentage points (ppts) (from +1.7ppts) to 10-year Malaysia Government Securities of 4.2%. — Kenanga Research, Jan 12

This article first appeared in The Edge Financial Daily, on Jan 13, 2017. Subscribe to The Edge Financial Daily here.

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Telegram

Latest publications

Follow Us

Follow our channels to receive property news updates 24/7 round the clock.

Malaysia's Most

Loved Property App

The only property app you need. More than 200,000 sale/rent listings and daily property news.