Jaks Resources Bhd (Jan 10, RM1.11)

Outperform with target price of RM1.50: Jaks Resources Bhd is one of the three Malaysian companies that have been awarded the independent power producer contract to build a power plant in Vietnam. The other two are Toyo Ink and Teknik JanaKuasa. As for progress, Jaks is arguably the most advanced as it has secured agreements which include a land-lease deal, a power plant agreement, build-operate-transfer (BOT) contract, coal-supply agreement and a government guarantee.

More importantly, it has roped in an established power plant builder, China Power Engineering Consulting Group Co Ltd (CPECC), as its equity partner to build a 1,200mw coal-fired power plant in Hai Duong province, Vietnam.

The joint venture (JV) company has also secured US$1.4 billion (RM6.26 billion) in financing, or 75% of the project cost. Works commenced in the second quarter ended June 30, 2016 (2QFY2016), with the first phase to be completed by 2020. We expect its near-term earnings to be underpinned by its Vietnam engineering, procurement and construction (EPC) contract worth RM1.9 billion, and other local jobs such as Sungai Besi-Ulu Klang Elevated Expressway (RM508 million), while recurring income to start kicking in by 2020.

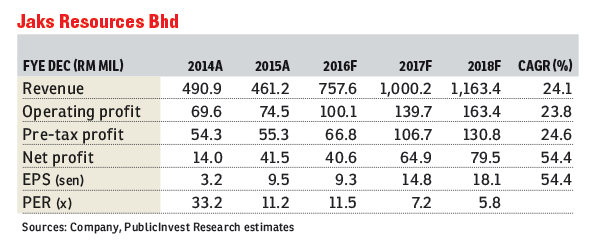

Our fair value is RM1.50, derived from about 30% discount to our sum-of-parts (SoP) estimates of RM2.20, or implied about 10 times of earnings per share (EPS) in the financial year ending Dec 31, 2017 (FY2017). Granted, earnings are bumped up mainly by its high-margin EPC contract but we believe the power plant financing structure is essential to ensure healthy cash flow and balance sheet during the construction period. Its net gearing is at 0.8 times currently, but should be pared down with the plan to dispose of its non-core assets.

Jaks, together with CPECC, is constructing a BOT power plant, with an estimated cost of US$1.87 billion with 25-year concession and power purchase agreement with Viet Nam Electricity. US$1.4 billion was already secured back in September 2015 from Industrial and Commercial Bank of China, China Construction Bank Corp and Export-Import Bank of China. The JV has US$160 million capital (equity portion) and expects the remaining balance of US$307.1 million to be injected in the next three years. Management expects strong internal rate of return with the first unit expected to be completed by mid-2020, and the second unit six months later. — PublicInvest Research, Jan 10

This article first appeared in The Edge Financial Daily, on Jan 11, 2017. Subscribe to The Edge Financial Daily here.

TOP PICKS BY EDGEPROP

Oasis 2 @ Mutiara Heights Kajang

Kajang, Selangor

Tropicana Indah (Damansara Indah Resort Homes)

Tropicana, Selangor

Isle of Kamares, Setia Eco Glades

Cyberjaya, Selangor

Bandar Baru Sungai Buloh

Sungai Buloh, Selangor

{kind=link}