M-REIT sector

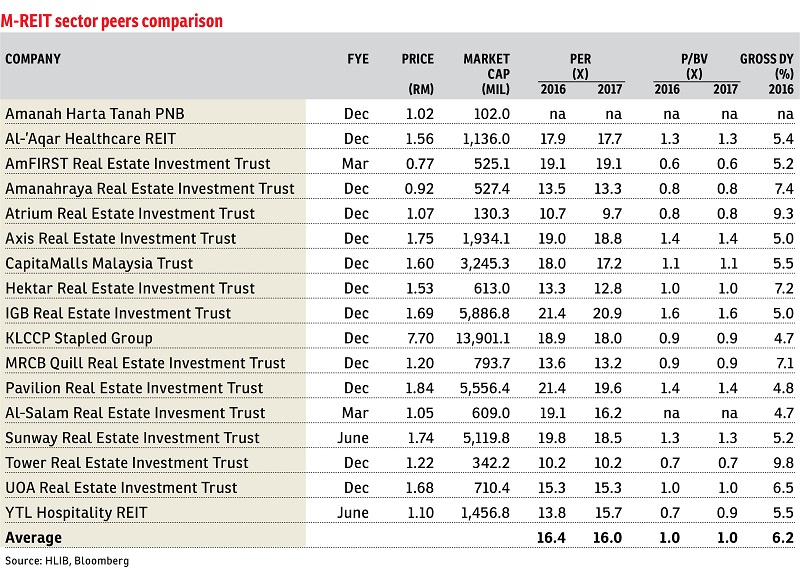

Upgrade to overweight: Much to our surprise, Bank Negara Malaysia (BNM) cut the overnight policy rate (OPR) by 25 basis points to 3% and we believe this will continue to spur the market to move into yield assets, and Malaysian real estate investment trusts (M-REITs) are often the darling of equity investors during monetary easing due to their stability and high-yielding nature, despite the average yield being compressed to 6.2%.

Moving forward, we expect the potential downside for M-REITs from external factors to be limited, with no immediate risk of a narrowing yield spread given the monetary easing bias and their relative attractiveness amid a low-yield environment and uncertainties in the global market.

In line with our previous expectations, local consumption is getting a further boost from the expected interest savings resulting from the OPR cut and improved sentiment, on top of normalisation of the goods and services tax effect, festive seasons and measures to support disposable income, which are a relief to our earlier worry about softer rental reversion.

While lower interest rates lead to potentially lower interest expenses, we do not expect significant interest savings for M-REITs on their borrowings as the majority of their borrowings are in fixed rates, except for Axis REIT and CapitaLand Malaysia Mall Trust, whose exposure to the floating rate are about 50% and 25% respectively as of financial year 2015.

Another near-term potential catalyst for the sector is the possible revision of REIT guidelines by the Securities Commission Malaysia to allow for green development up to a certain percentage of total asset value, similar to Singapore and Hong Kong, which allow development up to 25% and 10% of total value respectively.

Catalysts include: i) potential acquisition of quality assets to achieve growth as the softer property outlook presents such opportunities; ii) higher disposable income may spur retail spending, which will in turn boost retail REITs; iii) regulatory intervention in limiting the supply for offices and malls; and iv) a change in regulation with regard to green development.

In our view, risks to consider are: i) a prolonged erosion in consumer sentiment; ii) failure to execute planned asset injections and strategies; and iii) a significant slowdown in broad economic activities.

We upgrade the M-REIT sector to “overweight” on monetary easing bias with limited downside risk. The cautious outlook for the REIT sector is relieved by the accommodative monetary conditions, coupled with stability, attractive yield and sustainable interest among investors in the low global yield environment.

We revise our assumption of 10-year Malaysian Government Securities’ yield to 3.5%, from 4% previously, and valuations are based on a one-year historical average yield spread, in line with our house view on the possibility of further monetary easing in the near future.

Our top picks for the sector are MRCB-Quill REIT (target price [TP]: RM1.34), Pavilion REIT (TP: RM1.98) and KLCCP Stapled Group (TP: RM8.38). — HLIB Research, July 14

Want to know the price trends of a development? Click here.

This article first appeared in The Edge Financial Daily, on July 15, 2016. Subscribe to The Edge Financial Daily here.

TOP PICKS BY EDGEPROP

Jalan Setia Utama U13/38C

Setia Alam/Alam Nusantara, Selangor

Fortune Perdana Lakeside Residences

Kepong, Kuala Lumpur

Fortune Perdana Lakeside Residences

Kepong, Kuala Lumpur

{kind=link}