Kimlun Corp Bhd (June 30, RM2.27)

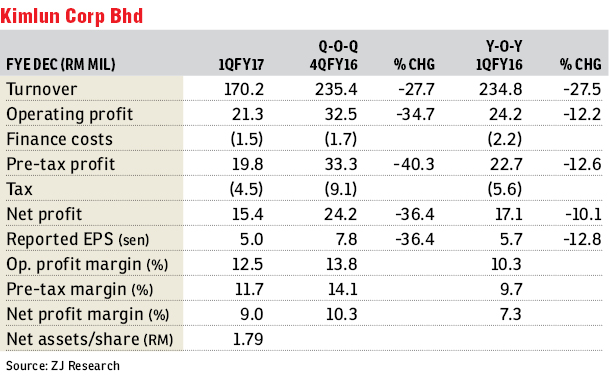

Maintain buy with a lower fair value (FV) of RM2.50: Following a strong performance in its financial year ended Dec 31, 2016 (FY16), Kimlun Corp Bhd kicked off FY17 on a softer note with revenue and net profit for the first quarter ended March 31, 2017 (1QFY17) falling 27.5% and 10.1% year-on-year (y-o-y) to RM170.2 million and RM15.4 million respectively. The results were slightly below our expectations. The variations were mainly due to lower contributions from both the construction and manufacturing divisions. Turnover and profit from construction business were down 21% and 14.6% y-o-y, while manufacturing recorded 53.2% and 47.3% y-o-y declines respectively.

Management clarified that the weaker performance was largely due to timing issue, as the group completed several larger-scale construction projects last year while the new jobs secured had yet to reach significant billing stage. Similarly, the manufacturing segment wrapped up the delivery of tunnel lining segment (TLS) for Singapore’s underground power transmission network as well as mass rapid transit (MRT) project, while the new contract to supply TLS and segmental box girders (SBG) for the Klang Valley MRT Line 2 will only pick up later this year. Sequentially, the drop in net profit was steeper at 36.4% quarter-on-quarter. Recall that there were some large variation orders recognised in 4QFY16 and the absence of these in 1QFY17, coupled with the lower revenue, contributed to the decline in profitability. On a brighter note, net gearing improved further to 0.04 times as at end-March 2017 from 0.07 times three months earlier, backed by a book value per share of RM1.79. The group also generated a positive net operating cash flow of RM32.9 million in 1QFY17.

Following the 1QFY17 results and having updated our earnings model parameters, we trim our FY17 earnings estimate by 11.9% to RM74.5 million. We also introduce our FY18 revenue and net profit projections of RM1.12 billion and RM83.7 million, respectively. Despite the soft 1QFY17 results, we remain positive about the outlook for Kimlun in the longer term. Earnings are supported by a healthy order book of RM1.59 billion for construction and RM330 million for manufacturing. The combined order book of RM1.92 billion would provide earnings visibility to Kimlun for the next two years. We expect earnings to trend upward again in FY18 as construction billings pick up pace and supply of TLS and SBG to MRT Line 2 ramps up.

On May 8, Kimlun announced that its newly incorporated 40%-owned joint venture company, JBB Kimlun Sdn Bhd, had clinched a RM263 million job from Astaka Padu Sdn Bhd to construct one block of office complex for Johor Bahru City Council. The job is scheduled for completion within 30 months from site possession date. No dividend was declared for the quarter under review.

We maintain our “buy” recommendation on Kimlun but lower our FV marginally to RM2.50 (from RM2.58), as we roll over our FY18 fully diluted earnings estimate and peg it with a target price-earnings ratio multiple of 11 times (unchanged). We like Kimlun for its prudent and proven leadership, healthy fundamentals as well as good track record in securing contracts. — ZJ Research, June 29

This article first appeared in The Edge Financial Daily, on July 3, 2017.

For more stories, download TheEdgeProperty.com pullout here for free.

TOP PICKS BY EDGEPROP

Setia Alam

Setia Alam/Alam Nusantara, Selangor

Setia Eco Park Phase 8

Setia Eco Park, Selangor

Taman Bayu Tinggi

Bandar Botanic/Bandar Bukit Tinggi, Selangor

Menara HLX (formerly Menara HLA)

KL City Centre, Kuala Lumpur

Merdeka 118 @ Warisan Merdeka 118

Kuala Lumpur, Kuala Lumpur

Bangunan Setia 1

Damansara Heights, Kuala Lumpur

Duduk Huni @ Eco Ardence

Setia Alam/Alam Nusantara, Selangor

Kuala Terengganu Golf Resort

Kuala Terengganu, Terengganu

Medan Idaman Business Centre

Setapak, Kuala Lumpur

{kind=link}