MMC Corp Bhd (April 4, RM2.49)

Maintain buy call with a target price (TP) of RM3.50: MMC Corp Bhd (MMC), Sime Darby Bhd and Adani Ports and Special Economic Zone Ltd (Adani Ports) signed a memorandum of understanding (MoU) to undertake feasibility studies with regard to the development of an integrated maritime city on Carey Island, Selangor.

Separately MMC and Adani ports also signed a MoU to explore the feasibility of the Carey Island port project as an extension of Port Klang. No timeline has been provided for the completion of these studies.

The maritime city is to support the proposed development of a new port on a greenfield site on Carey Island, located about 50km south-west of Kuala Lumpur.

Port Klang was ranked the 11th busiest port in the world in 2016, based on container throughput and trans-shipment volumes of 13.17 million 20-ft equivalent units (TEUs). We believe that growth in global trade should drive strategic new capacity expansion at Port Klang.

MMC currently owns four ports in Malaysia and all are strategically located along the Strait of Malacca. This is one of the most important shipping waterways in the world. It is the shortest shipping channel between the Indian and Pacific Oceans, linking major economies such as the Middle East, China, Japan and South Korea. Around 80% of the oil transported to north-east Asia and one third of the world’s traded goods pass through the strait every year.

In the event that the development of the port is given the green light, we believe it would require 10 to 15 years before full port capacity can materialise. Based on a report in The Edge Malaysia weekly (Feb 20-26) regarding MMC, the company is looking at a potential capital expenditure of RM20 billion to RM40 billion for the development of the Carey Island port and 10 million TEUs capacity.

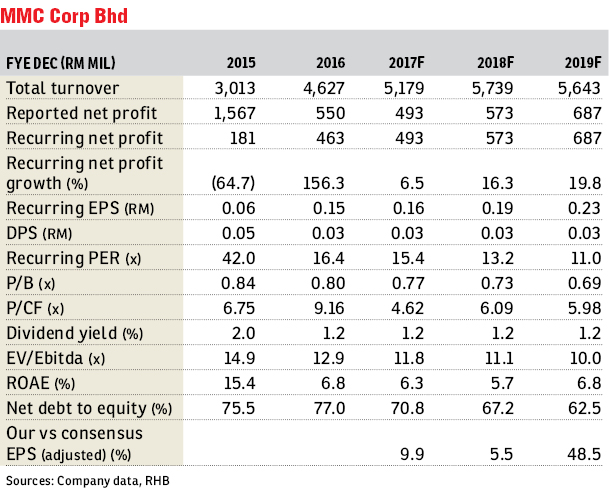

While MMC’s financial year 2017 (FY17) forecast net gearing of 71% is high, we are of the view that the company would have the balance sheet strength to undertake the project. This is given the potential listing of its port assets in 2018/2019 and joint ventures.

MMC is currently trading at a 72% discount to our sum-of-parts (SoP) valuation. We expect the company to generate earnings growth of 7% to 20% in FY17 to FY19, driven by operational and cost synergies from its ports division, resilient utilities demand and strong construction order book.

We maintain our “buy” call on the stock with a SoP-based TP of RM3.50. Key catalysts for the stock include the potential spinning off of its ports division and strong order book replenishment. — RHB Research Institute, April 4

This article first appeared in The Edge Financial Daily, on April 5, 2017.

For more stories, download TheEdgeProperty.com pullout here for free.

TOP PICKS BY EDGEPROP

Jalan Setia Utama U13/38C

Setia Alam/Alam Nusantara, Selangor

Fortune Perdana Lakeside Residences

Kepong, Kuala Lumpur

Fortune Perdana Lakeside Residences

Kepong, Kuala Lumpur

{kind=link}