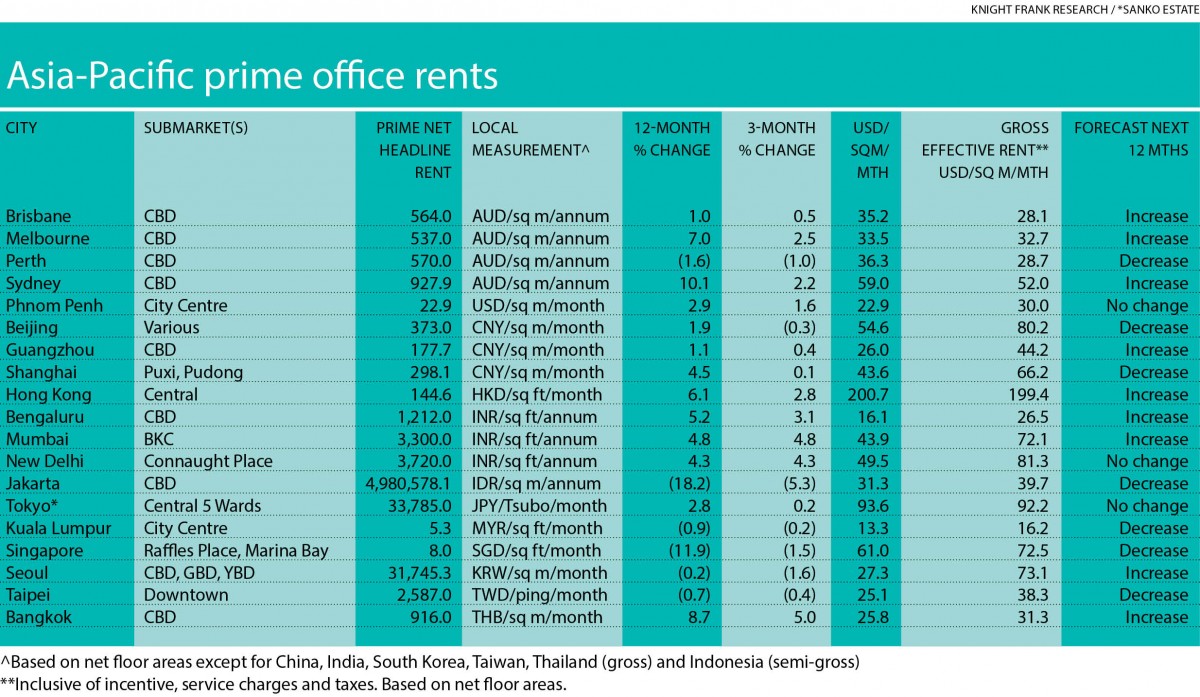

IN its latest Asia Pacific Prime Office Rental Index for 4Q2016, global property consultancy Knight Frank found that 12 cities out of 19 surveyed in the Asia-Pacific region have registered positive rental growth in 4Q2016, up from eight in the previous quarter. As a result, the rental index has increased 1.3% quarter-on-quarter (q-o-q) and 2% year-on-year (y-o-y).

Knight Frank expects rents in these 12 cities to remain steady or to increase further.

Despite the overall positive rental growth recorded in major cities in the region, international office occupier demand for office space continues to be dampened by a combination of softer external demand and tightening of global financial conditions. As such, the importance of domestic demand is rising amid the economic and trade uncertainty.

“Across the region, international companies are taking a cautious approach to mitigate the negative effects of an uncertain global economy. Increasingly, markets with robust absorption and sustained demand from a diverse group of local firms will continue to experience growth,” said Knight Frank Asia Pacific head of research Nicholas Holt.

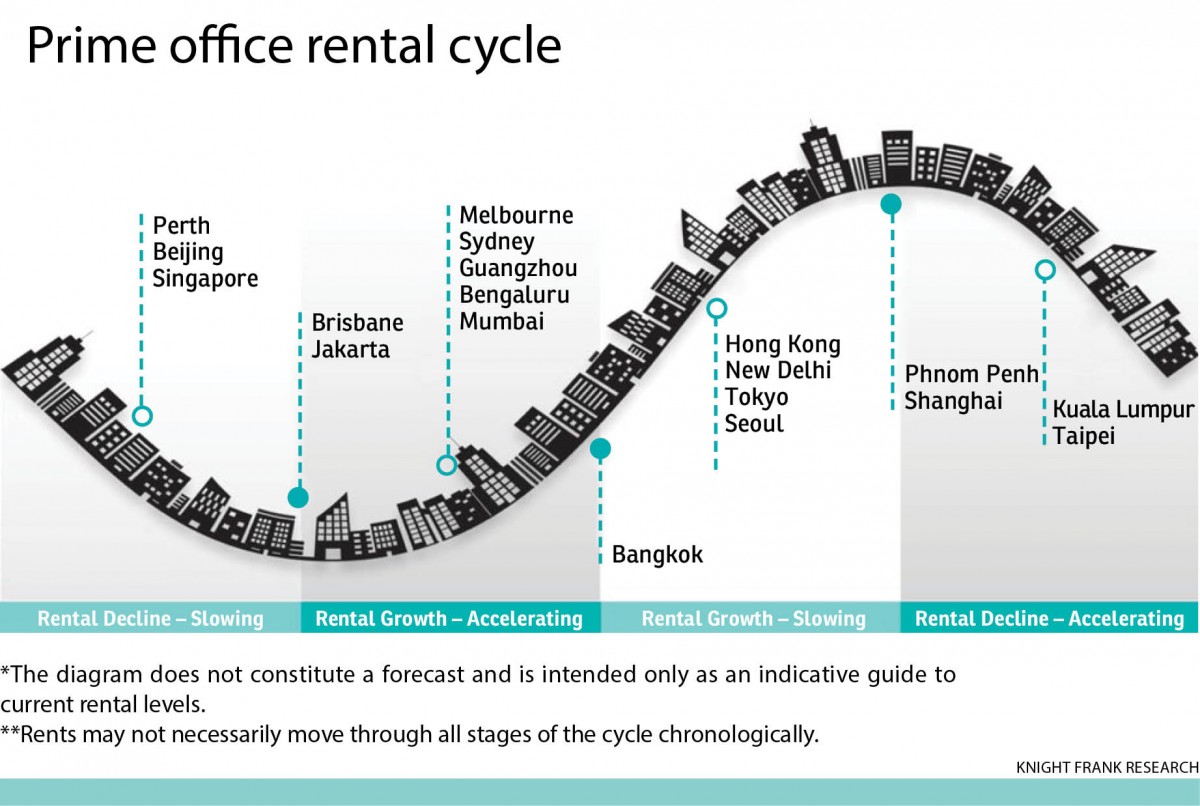

Based on the index, Bangkok was the strongest-performing office market across major Asia Pacific cities last quarter registering a strong growth of 5% q-o-q and 8.7% y-o-y. Rents have been on the rise in Bangkok since 3Q2014 due to limited high-grade office supply in the central business district where demand is expected to remain strong.

Despite global uncertainties, Indian cities occupying second, third and fourth places, respectively, on the rental index were Mumbai (4.8%), New Delhi (4.3%) and Bengaluru (3.1%) where supply struggled to catch up with robust demand coming from various sectors especially technology firms.

In Cambodia’s capital of Phnom Penh, office rents rose by 2.9% y-o-y while vacancy rates continued to decline.

Pressure on KL, Jakarta and Singapore office rents

On the other hand, the office markets in Kuala Lumpur, Jakarta and Singapore remained subdued in 4Q2016. As large incoming supply are in the pipelines in all three cities in 2017, the subdued demand will likely exert further downward pressure on rental and occupancy levels, said the consultancy.

According to the report, the rental index of KL, Jakarta and Singapore have decreased by 0.2%, 5.3% and 1.5%, respectively, in 4Q2016. Jakarta was the weakest performer registering a -5.3% change q-o-q.

")

")

Despite the growing mismatch in office supply and weaker occupier demand from the oil and gas sector, the KL office market has remained resilient, said Knight Frank Malaysia executive director of corporate services Teh Young Khean.

“The rental index decreased only 0.2% during 4Q2016 although it is expected to dip further in the near term,” Teh added.

Over in China, cities like Beijing, Guangzhou and Shanghai have seen their office vacancy rates increase. However, it was counterbalanced by strong domestic demand, causing rental movement to remain minimal in 4Q2016.

The report noted that Shanghai and Beijing will see close to 2.9 million sq m and 0.6 million sq m of prime space coming into the market in 2017, respectively.

In Hong Kong, prime office rents have grown for the eighth consecutive quarter, with a growth of 2.8% in 4Q2016.

“Looking ahead, the uptrend for office rents on Hong Kong Island is likely to continue in 2017, with Central set to outperform the wider market, given the tight availability of space,” noted the report.

Elsewhere in East Asia, office markets remained stable where rents in Taipei slid slightly by 0.4% while rents in Tokyo remained flat. In Seoul, prime rents dipped marginally q-o-q to a level similar to a year ago.

Meanwhile, rents continued to rise in Australia except for Perth, where vacancies and incentive levels were close to the bottom.

On a y-o-y basis, Melbourne and Sydney witnessed rental increases of 7% and 10.1%, respectively, while in 4Q2016, the rental index of the former and latter had increased by 2.5% and 2.2%, respectively.

“With falling vacancy rates, landlords are offering less incentives in these cities. Rents in Brisbane have not declined since 2Q2015, signalling a possible recovery.

“The services sector, including technology and creative industries, will continue to drive leasing activity in Australia in 2017,” said Knight Frank.

This story first appeared in TheEdgeProperty.com pullout on March 17, 2017. Download TheEdgeProperty.com pullout here for free.

TOP PICKS BY EDGEPROP

Armani Kajang Industrial Park

Kajang, Selangor

Palm Hill Residence 2 (Residensi Bukit Palma 2)

Cheras, Selangor

Damansara Heights (Bukit Damansara)

Damansara Heights, Kuala Lumpur

Bandar Sungai Long

Bandar Sungai Long, Selangor

{kind=link}